The Polish funding ecosystem has been blossoming over the past few years.

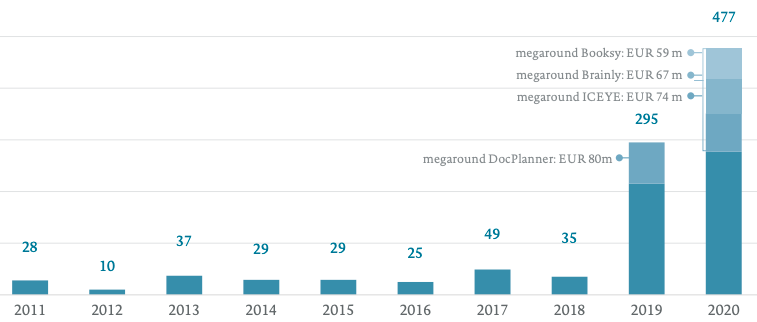

Chances are, you have heard of startups like DocPlanner, Brainly, Packhelp, Booksy, or Uncapped. Those companies have amassed substantial financial firepower from investors and are actively pursuing the status of first Polish unicorn. In the first two quarters of 2021, Polish startups have raised €260 million which sets the bar for a record-breaking year. Total VC funding in Poland grew 8x (!) from 2018 to 2019 and 1.6x from 2019 to 2020.

For perspective - before 2019, the whole Polish VC market was comparable in size to a single B round in the US (Source: PFR Ventures).

So what happened exactly?

Public money fuels the growth of Polish VC

Government contributions are instrumental in the Polish funding ecosystem. That is visible in both equity funding as well as non-equity support. The three most prominent public players are:

- PFR - Polish Development Fund - a government-dependent financial group aiming to support the development of local companies and support economic growth. Within the group, there are PFR Ventures (the largest Polish fund of funds) and National Capital Fund (a historical predecessor to PFR Ventures) - the primary capital providers (and oftentimes anchor-investors) to the vast majority of VC funds in the country.

- NCBR - National Centre for Research and Development - a government agency aiming to create and support innovative technological and social solutions in Poland. They offer a wide range of equity-free grants like "Fast track" and act like an LP in many local (nano-) funds.

- PARP - Polish Agency for Enterprise Development - a government agency aiming to implement economic development programs mostly dedicated to Polish SMEs. They offer both equity-free incubation as well as acceleration programs, grants, or even programs dedicated to foreign startups like Poland Prize . All of those are free and aimed at early-stage projects.

Startup Poland foundation reports that the local startup success rate in raising a venture round is 32% while the chances of winning a grant application are 69%. Out of those who raised venture capital, 32% were already backed by PARP and 16% by NCBR. By the way, chances are that PFR was the main investor in the VC funds that deployed that venture capital.

A suction effect for local and international capital

The stimuli created by PFR and NCBR led to an increase in the number of active VC funds in Poland, from 43 in 2016 to around 100 today. While the majority of them are heavily supported by the state, there are a bunch of bigger funds that have the EIF (European Investment Fund) and private investors on board. They are also the ones that focus on the later rounds and invest internationally. Here are a bunch of funds that would be the primary targets for startups with no intention to establish a Polish entity: OTB Ventures, Market One Capital, Inovo Venture Partners, Innovation Nest.

As a consequence, we're starting to see big rounds drive up the total investment numbers. According to PFR and Dealroom in 2020, there were 26 Series A investments and 6 Series B and further.

Those bigger deals are a honeypot for international capital. In 2020, only 13% of the deals were made by foreign investors but their contribution to the total transactions value was a whopping 48%. A similar pattern can be observed in 2021.

Another important vertical is angel investing. While startups as an asset class are not that popular in Poland, the number of angels is growing. This is partly due to the success of syndicates, that are widely regarded as the best place to angel invest successfully.

The momentum of Polish VC has yet to be confirmed

There's only so much public money can do. Now that the pump has been primed, Polish VC will have to face the structural challenges that prevented it from growing in the first place.

First of all is the lack of local institutional LPs. Due to the inflexible nature of the local pension system, pension funds do not invest in venture capital at all. Private LPs are primarily represented by high-net-worth individuals and family offices, which, because of the relatively young history of capitalism in the country, are not fully developed yet.

Consequently, local VCs are bred by PFR and NCBR and are bound to invest in Polish entities only, undergo formal procedures to approve investments, and commit small checks, usually below €1 million. This is by no means optimal or competitive compared to more advanced ecosystems. However, it is not to say that this support is not needed. It is hard to imagine the budding venture capital space in the country without public backing.

Another obstacle lies within angel investing. In comparison to the UK or Germany, the tax benefits of angel investing are far less prominent and excessive red tape hinders the transaction speed. Our mission at COBIN Angels as the largest professional angel network in Poland is to lift up those bottlenecks. Our structure has been designed to minimize red tape and our 100% private funding allows us to react fast and be flexible. Ultimately, we want to provide the best possible angel investing experience for both investors and startups.

Now is the time for private initiatives to take over public efforts. As more domestic and foreign capital gets poured into Polish startups, we can only hope that regulations will follow suit and unlock a bright future for Polish VC.

About the author

Bohdan Mashtalir is an Associate at Inovo Venture Partners. Bohdan can be reached at [email protected]

.

Resources

-

Overview of the Polish VC ecosystem by VC Leaders

-

Cobin Angel Field Guide that lists down Polish accelerators and VCs

-

NCBiR grant programs list

- List of programs run by PARM

- List of PFR-backed funds

OpenVC is the best way to access deals 🤝

Browse the top 1% of deals and interact directly with founders. Completely free.