Two things are true for seed stage VC investing relative to later stages.

- Companies’ prospects of success are less certain.

- There are more companies to choose from since most have not had time to fail.

By the time companies make it to needing growth stage capital, the growth stage VCs will have greater certainty about which companies are likely to provide the greatest returns. The key to success for growth stage VC investing is getting into these promising deals, which requires rubbing shoulders and jostling elbows.

Early stage investing is more collaborative. The key to success for early stage VC is to pick winners based on limited information.

So what's the optimal VC strategy to pick winners?

Table of Contents

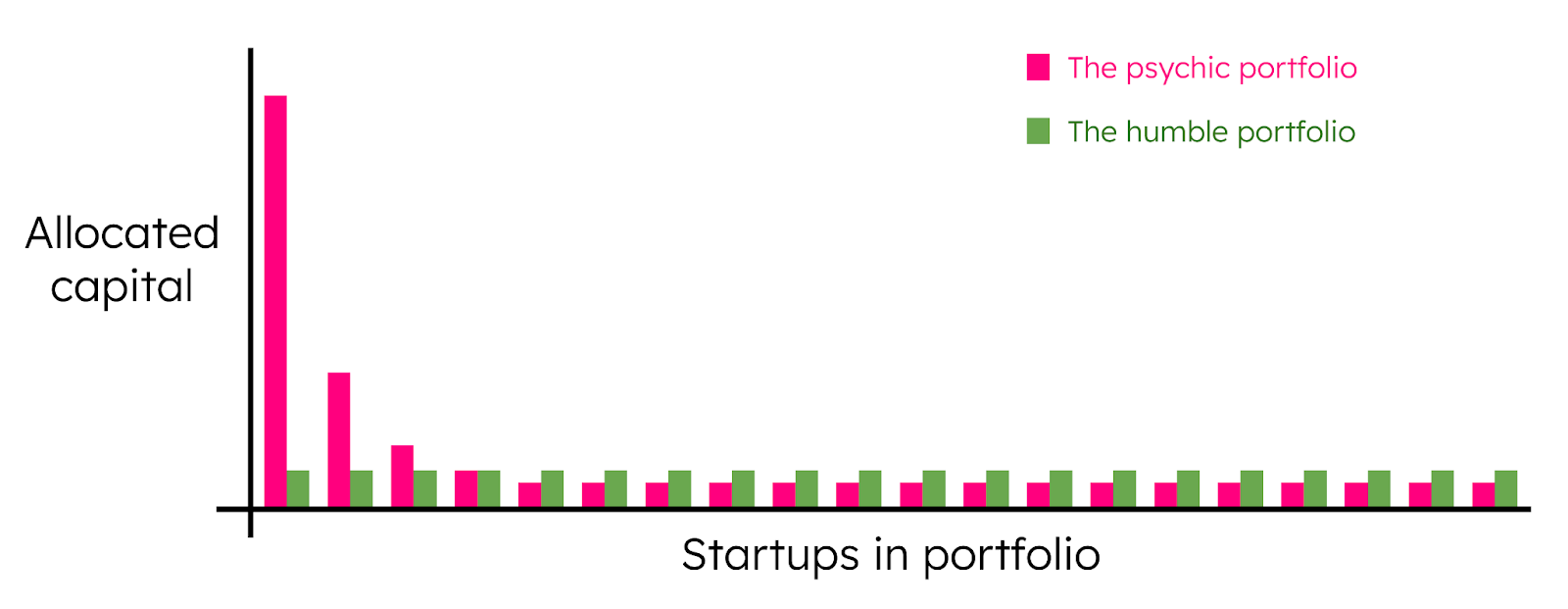

"Spray and pray" vs. "Big bets"?

Two philosophies abound. See Rodrigo Ferreira’s post from March 2022. One says that it is better to have a small stake in many possible winners to avoid a high probability of missing out. The other approach says that the best portfolio is one with all the money in the biggest winner, and diversification is just a hedge against uncertainty about which deal that is.

In reality, the best balance between diversification and conviction is somewhere between one deal and every possible deal. How to choose? Portfolio concentration should be proportional to knowledge. The more one knows, the more likely one is to pick the winners.

Being familiar with (a) the field of technology or science of a company’s products and (b) the target market space are helpful. This need can be filled by broadly knowledgeable advisors. Or, even better, a large Rolodex of people with deep expertise.

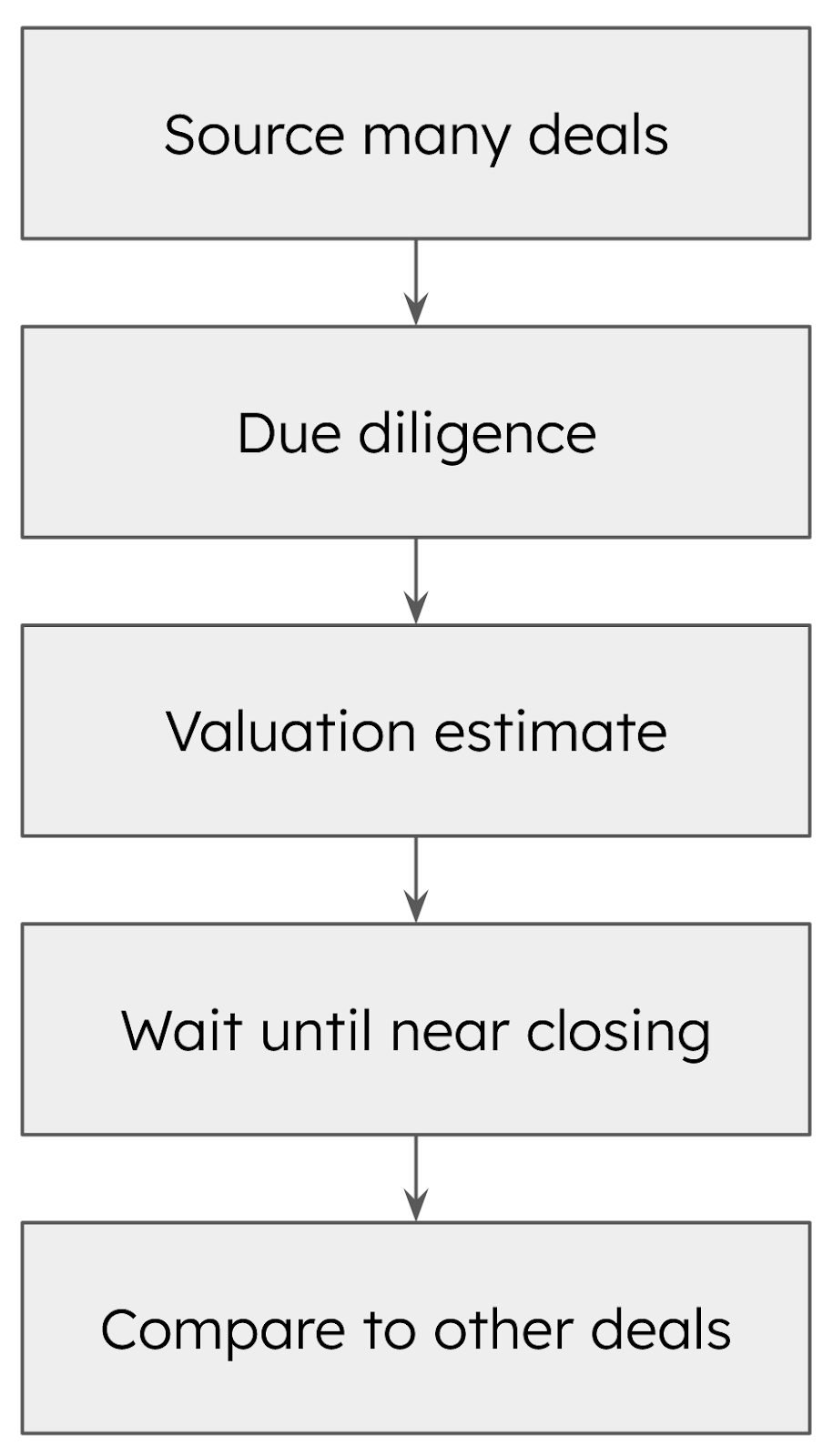

Due diligence is important

Even more helpful is insightful due diligence. Even a moderately ignorant investor can identify the biggest risks by asking the right questions in the right ways.

One technique is to ask open-ended questions. Those are questions that require more information than a yes or no answer. Open ended questions usually begin with the word who , what , when , where , why , or how. For example, don’t ask founders, “ Are you sisters? ”. Instead ask, “ How do you know each other? ”. They might be cousins.

Look at options in the context of others

Knowledge increases over time. Procrastination is valuable. Committing to an investment decision at the last moment allows for both (a) discovering problems before it is too late and (b) inferring the opportunity cost.

Every investment has an opportunity cost. It is the value of the best deal that will get passed on in the future deployment period of the fund.

Interestingly, uncertainty weighted opportunity costs decline throughout the life of a fund as there are ever fewer yet unseen deals. The decline is useful in constructing a portfolio of later stage companies. However, it is not very useful for seed stage investing because the inherent uncertainty of any seed stage investment is so much higher than that of a better future deal that it is hardly worth considering.

Still, at any given time, a fund manager should sort all visible deals in order of a best estimate of their uncertainty weighted value. As the deadline to commit arrives for each deal, the fund manager should invest if the deal is in the top D*(W/T) visible deals where D is the number of investments remaining to be made from the fund, W is the time window of visibility into deals, and T is the time remaining in the deployment period.

Consider a fund with a 30 month (2.5 year) deployment period.

Suppose, simplistically, that every deal has a 3 month window from when it is discovered until the deadline to commit (W=3). If a deal deadline arrives at month 18, 12 months remain in the deployment period (T=12).

If, at that time, the fund has capital left to deploy into 16 deals (D=16), the fund manager should invest if the deal is in the top 4 available deals. 16*(3/12)=4

Many investors look at each deal individually. Optimal investment picking considers each deal in the context of all other available deals.

Teamwork gives good outcomes

Sometimes the most helpful deal insight of all, when presented with insufficient other information, is the consensus of other investors. This is why early stage VCs are more collaborative than competitive.

VCs are sometimes described negatively as acting in herds. But the aphorisms of safety in herds and strength in numbers are both true. A herd is safer because there are more eyes looking out for danger. There is strength in numbers because a larger number of investors are more likely to be able to bring in later stage investors to support the company.

Conclusion

Success in seed stage investing requires picking winners from a large number of deals with limited information. Two approaches exist - taking small stakes in many startups vs. concentrating on the biggest winners. The right balance depends on knowledge. Knowledge of the technology and market, good advisors, and probing due diligence help. Information to inform a decision is available from context. Investment decisions should be made while looking at an array of available deals. Ultimately, however, consensus with collaborative investors can be most important for the success of any given deal.

OpenVC is the best way to access deals 🤝

Browse the top 1% of deals and interact directly with founders. Completely free.

About the author

Jonah Probell is Managing Partner of Lexi Ventures. Lexi is seeding the coming wave of genomics and synthetic biology, which will cure every major disease, change the things we see, touch, and eat, and heal the planet.

Jonah co-founded 2 and worked for 7 startups with 2 IPOs. He developed views on rational portfolio construction in the context of large patent portfolios. He has written two books on the topic.

![12 Best Startup Financial Model Templates [Free & Paid]](https://d1pnnwteuly8z3.cloudfront.net/images/177302d9-3657-45b7-ac9d-acf801d83a74/1b029edf-43cf-4bd9-9e37-203f66bf426f.png)