This post is part of a series on structuring the team and legal infrastructure of a new VC fund. Next post coming out in a week!

If you are launching your own investment management firm, we recommend designing a “constitution”: a set of documents covering the firm’s goals, legal obligations, and principles for handling disagreement. Coolwater Capital, the “Y Combinator for VC funds,” assesses this as part of the diligence process. And at Orrick , we assist fund sponsors with preparing their “constitution.” David Teten

is now building a new VC fund and using this framework in structuring relationships with anchor investors and Partners.

Table of Contents

Why you need a constitution for your VC fund

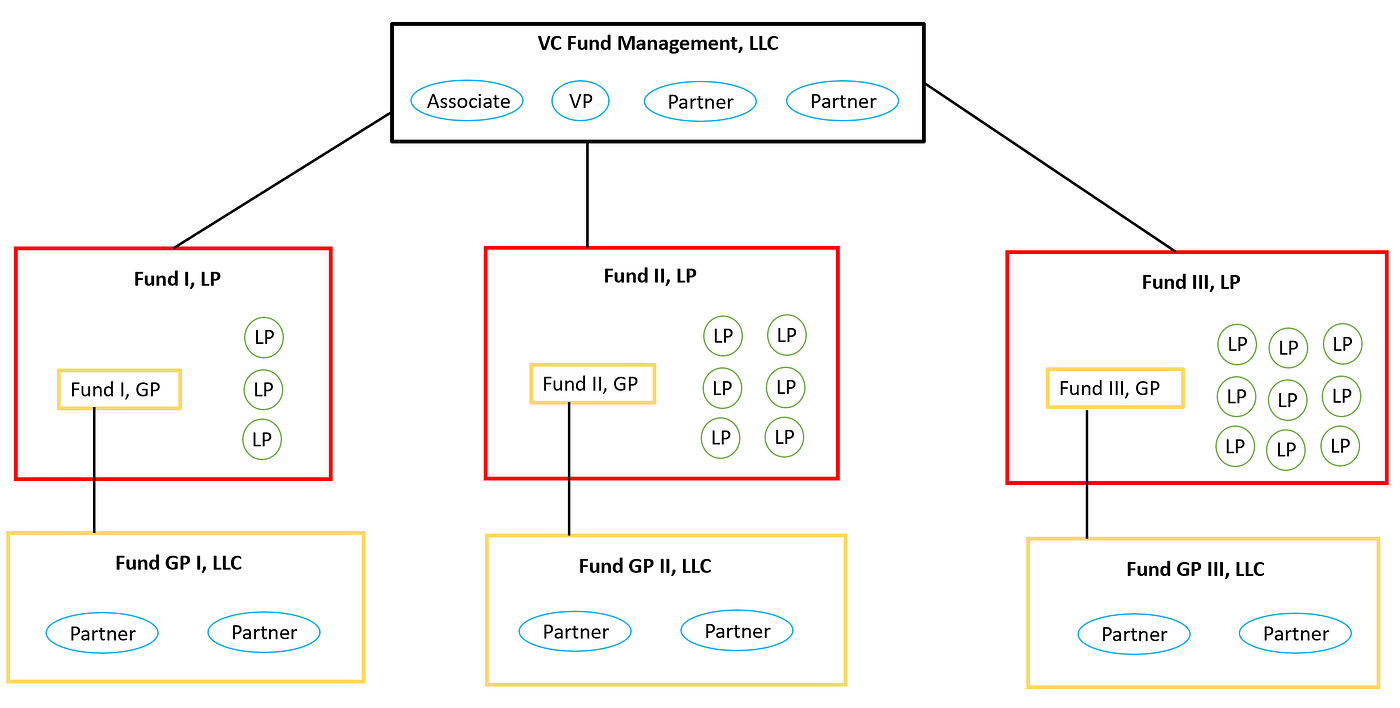

The most important documents for a new firm are the agreements governing the general partner entity and the management company entity, which may include co-founding partners, anchor investor, and early employees. These entities are essential for managing the fund and profits, and complying with legal and tax requirements.

However, forming your new fund also typically requires making important decisions about firm strategy, culture, how you make decisions, budget, data ownership, and other issues. These agreements may be inappropriate, unfeasible, or unwise to put in your signed legal documents. It’s hard to address these issues in such a black & white way that they’re readily enforceable. However, that doesn’t mean these issues are unimportant.

Any agreement can be renegotiated if the parties are willing. That said, the process of negotiating the initial design of the firm, even though it will inevitably change, is a valuable forcing function.

Part of the challenge is that the best partnerships are made of complementary, heterogeneous people. It requires more upfront work to structure the partnership among a diverse group, but the group becomes a more valuable team once launched. Brian Cohen, Chairman, Six Point Ventures, observed, “Multiple partners with different primary skill sets are mandatory. Otherwise there is too much second-guessing and not enough professional trust.”

We’ve listed below all the major non-legal issues to consider.

Strategy

The team should collectively align on the investment focus, differentiation, and long-term aspirations. See 33 Questions We Asked Ourselves Before Starting Pace Capital and Alexander Jarvis’s collection of investment theses.

“The General Partner shall focus his/her investment activities on [sectors, geographies, types of companies]. The firm’s long-term goal is [long-term aspirations].”

Culture

Miles Lasater, CEO and Founder, Purpose Built, said, “As VCs, we know the importance of evaluating team dynamics before we make an investment. Yet, we sometimes forget to bring that insight to building our own organizations.”

For a discussion of how to assess culture in Ready to Join a New Management Team? Here’s How to Do Your Due Diligence First. Ideally, the fund will have a public statement of culture (see, e.g., Antler, Interlace Ventures ). Even if unpublished, documenting your cultural norms will inform decision-making.

“The General Partner shall adhere to the following cultural principles: [ cultural principles such as integrity, transparency, innovation, etc.]. ”

Decision-Making

Dave Perretz, Founder at TheFundCXO, said, “Institutional LPs will examine your decision-making processes. A team constitution is a sign of maturity of a business and will save a lot of headache down the road.”

Most importantly, clarify if there’s a unitary CEO/leader. If not, then you should explicitly say that there are two equal leaders, although that model tends not to scale very well. In general, we suggest that the co-partners clearly delineate responsibilities against all of the business’s functions. We suggest in each function, one of the co-partners acts as the lead, while the other co-partner reserves the right to “ disagree and commit.” For example, one partner might be acting CFO and is the decider on financial management issues. She is expected to ask for counsel from other partners as appropriate.

Disagreements are inevitable in any organization. Establishing clear decision-making mechanisms is crucial for smooth operations. In the day-to-day running of a firm, if you’re looking at your legal documents to see the rules of how you and your co-partners are to make decisions, you likely have a bigger problem. Normally, decisions are made via dialogue and consensus, regardless of what the firm’s operating agreement may say.

Sometimes “ Structured Debate ” can also help your team raise and address competing priorities or points of view in a constructive way. This is done by randomly assigning different team members to argue opposing points of view.

“Decisions shall be made by consensus among the Partners. In the event of a lack of consensus, the partners holding a majority of the “carry stake” shall make the final decision.”

Budget

Determining the team size, compensation levels, and office policy is essential for budgeting. See Templates and Resources for Modeling Venture Funds. We suggest creating a draft budget based on achieving your target AUM, but also on achieving half your target AUM. It’s a healthy decision to plan for the downside.

Expense Policy

What tier of hotel will you stay in? Do you normally fly first class or coach?

“Each Partner may spend up to $[amount]/month unilaterally. Expenses above this level require approval from at least one other Partner. The firm shall adhere to the following T&E policies: [tier of hotel, class of flight].”

Further reading:

Social Media Policy

Are you comfortable with your colleagues posting this selfie on LinkedIn?

What’s your policy about communicating via blog, social media, etc.? How about on politics?

“Partners are [encouraged] [discouraged] from engaging in public communication via blogs, social media, etc. Any material public communication related to the firm or its investments must be approved by [designated person or committee].”

Further reading : An Investor’s Personal Social Media Tech Stack: In the future, everyone will be famous for 15 followers

Data Ownership

Who controls dialogue with each portfolio company? With limited partners?

Does the firm have a CRM system ? Are all team members required to put all data into it?

What happens when someone leaves the firm? Do they get to download the data regarding the people and/or companies with whom they were in contact? Giving this permission reduces the incentive to create a personal data solo.

“All data related to portfolio companies and limited partners shall be stored in the firm’s CRM system. Upon leaving the firm, individuals [may]/[may not] download or retain any data from the CRMwithout explicit permission from the [General Partner].”

Peaceful Resolution Agreement

Shane Ray Martin, Investor, B Ventures Group, suggests that partners create a peace agreement to allow for the option of a 24-hour pause before addressing contentious issues. After this reflection, both parties agree to reconvene. This helps prevent escalation, lawsuits, or strained relationships.

“In the event of a disagreement between co-partners, both agree to a 24-hour reflection period before reconvening to address the issue. ”

Future Funds

It may seem premature to worry about future funds when you’re just launching Fund I, but initial discussions about future funds can be beneficial. For example: What fund size is a realistic goal? What fund size would motivate your colleagues to stick around instead of looking for a job elsewhere?

“The co-partners shall periodically review and discuss the potential for launching subsequent funds. These discussions shall consider the performance of the current fund, market conditions, and strategic goals.”

Other helpful resources

Websites:

- How To Make Calculated Decisions When Forming Your GP Entity

- Fundamentals of fund formation: structuring the upper tier

- Venture Capital Fund Mechanics - VC Lab

- ILPA Private Equity Principles | Institutional Limited Partners Association

- Venture Capital Investment Committees: Best Practices From Elite VC Firms

- Operational excellence: one path or many

- A Look Under the Hood of Venture Capital Firms | by Trey Calver

- Budgeting the Management Company of a Venture Capital Fund | Foresight

Books:

- Amazon.com: The Venture Fund Blueprint: How to Access Capital, Achieve Launch, and Actualize Growth, or The Venture Fund Blueprint

- The Business of Venture Capital: The Art of Raising a Fund, Structuring Investments, Portfolio Management, and Exits (Wiley Finance)

- How To Raise A Venture Capital Fund: The Essential Guide on Fundraising and Understanding Limited Partners

- Starting Your Own Venture Investment Fund: A How To Guide: Moore, Kevin Joseph

Thanks to Jon Weber, Erik Brue, Shane Ray Martin, and coach Ben Dattner for thoughtful input.

About the authors

David Teten is the founder of Versatile VC, which backs “investment tech” companies which help investors generate alpha. He is a Venture Partner with Orange Collective, a fund of 150+ Y Combinator alumni backing Y Combinator founders. David is Chair of AltsTech, a community of investors in private companies using AI, technology and analytics to generate alpha, and Founders’ Next Move, for tech founders exploring new ideas. He was formerly a Partner with Coolwater Capital, which invests in emerging fund managers as a limited partner, into general partnerships, and into fund management companies. He was also formerly a Managing Partner with HOF Capital; Partner with ff Venture Capital; and Founder of Harvard Business School Alumni Angels of NY. He started his career as a strategy consultant, Bear Stearns investment banker, and serial founder with 2 exits as CEO.

Dolph Hellman, a leading fund formation and commercial finance lawyer in the San Francisco office, is the Co-Chair of Orrick’s Private Investment Funds Group and a member of the firm's Corporate Department. Dolph concentrates his sophisticated practice on private equity investor representation and fund formation as well as representing financial institutions and corporations in privately negotiated debt transactions. In addition, Dolph has a broad range of experience in commercial lending transactions, including secured financings, unsecured and asset-based financings, vendor and customer financings, subscription credit facilities, project financing, venture debt financings, letters of credit, receivables purchase financings and leasing.