A startup exit is one of those things that make being a founder sound like a dream. It’s the picturesque image of success most would-be founders imagine when they start building a company. A massive payout, a big headline, maybe a splashy champagne toast.

But if you’ve not been through it before, here’s what no one tells you: it will likely feel less like a victory lap, more like a high-stakes rollercoaster.

Most guides will walk you through the basics of M&A mechanics, but they rarely tell you the things that actually make a difference when you’re in the trenches. These are the insights I wish I had known, read, heard, or picked up while I was still grinding to build my first startup, and long before it sold for $780M.

Table of Contents

Bankers are major intel hubs.

First impressions might lead you to view bankers as transactional players who come in at the last minute to “sell” the company. That’s a mistake. The right investment banker can do so much more than make deals.

Great bankers have a finger on a pulse that VCs and startups often aren’t even aware of. They know who’s actively looking to acquire, which competitors lost out on previous deals and may be hungry to buy, and what industry shifts are making certain acquisitions more urgent. And they can use all this insider info to position your company correctly, maximize perceived value, and bring multiple bidders to the table.

If you wait until you’re actively selling to hire a banker, you’re missing out. By then, it’s too late for them to shape the way your company is positioned in the market.

At Vungle, we engaged with bankers well in advance. They helped us craft the right narrative. Because of this, we knew to position the company as an essential piece of a larger industry trend rather than just another ad-tech startup. That earned us more interest, more competitive tension, and ultimately, a better deal.

Given this info, what should you be adding to your action items? Consider these:

- Connect with investment bankers before you need them. Yes, even if you feel you’re still lightyears away from even considering selling. Staying on their radar can give you invaluable market insights.

- If an exit is on the horizon, start working with bankers ASAP to refine your company’s positioning before you're in active deal talks.

Warm up to senior executives instead of CorpDevs.

A common misconception among founders in acquisition mode is that corporate development (Corp Dev) teams are the ones who decide whether to buy your company. In reality, Corp Devs don’t drive acquisitions. Senior executives do.

Corp Dev is responsible for executing deals, but they don’t have the authority to just wake up one day and say, “We’re buying this company.” They need internal champions: senior leaders within the company who see your business as critical to their strategy. These champions could be the CEO, a head of product, a sales executive, or even a general manager in charge of a new initiative.

So how do you get those champions?

You play the long game. At Vungle, we actively built relationships with executives inside multiple potential acquirers.

Take Microsoft as an example. At the time, our ad platform worked only on iOS and Android, but Microsoft was pushing to grow its Windows app ecosystem. We structured a partnership where they paid us an eight-figure development fee to bring our product to Windows.

This did two things:

- It made us strategically valuable to Microsoft because we were solving a real business problem for them.

- It put us in front of high-level decision-makers. And I’m not talking mid-level managers here. Think SVPs — we even met Satya Nadella.

That kind of access changes everything when acquisition discussions start. Corp Dev moves faster when they already know you and when senior executives inside their company are championing the deal.

Here’s how you can execute this in your own company:

- Forget about selling for now. Just focus on partnerships. Find ways to work with large companies in ways that make you valuable to their core business. And on that note…

- Make sure you’re essential, not optional. If your company’s success directly benefits theirs, you become a natural acquisition target. (More on this in my next pointer).

- Identify key decision-makers, not just Corp Dev. Look for executives in product, sales, or general management who have a reason to engage with you.

- Keep the relationship warm. Stay in touch, keep providing value, and ensure that when M&A discussions do happen, you already have champions inside the company.

Don’t just talk EBITDA. Sell the combined entity’s future value.

If you’re negotiating an acquisition based on revenue multiples or EBITDA, you’re doing it the “right” way. And that’s how you end up with an average deal.

A more powerful play is showing the acquirer how much more valuable your company will be inside their ecosystem.

This brings to mind our experiences in discussions with a major tech company (not Microsoft, but let’s just say they’re a household social media name). At that time, we worked with their team to model how much revenue our product could generate once it had access to their massive sales force.

The result? We weren’t just a $100M revenue business. We were a multi-billion-dollar opportunity for them.

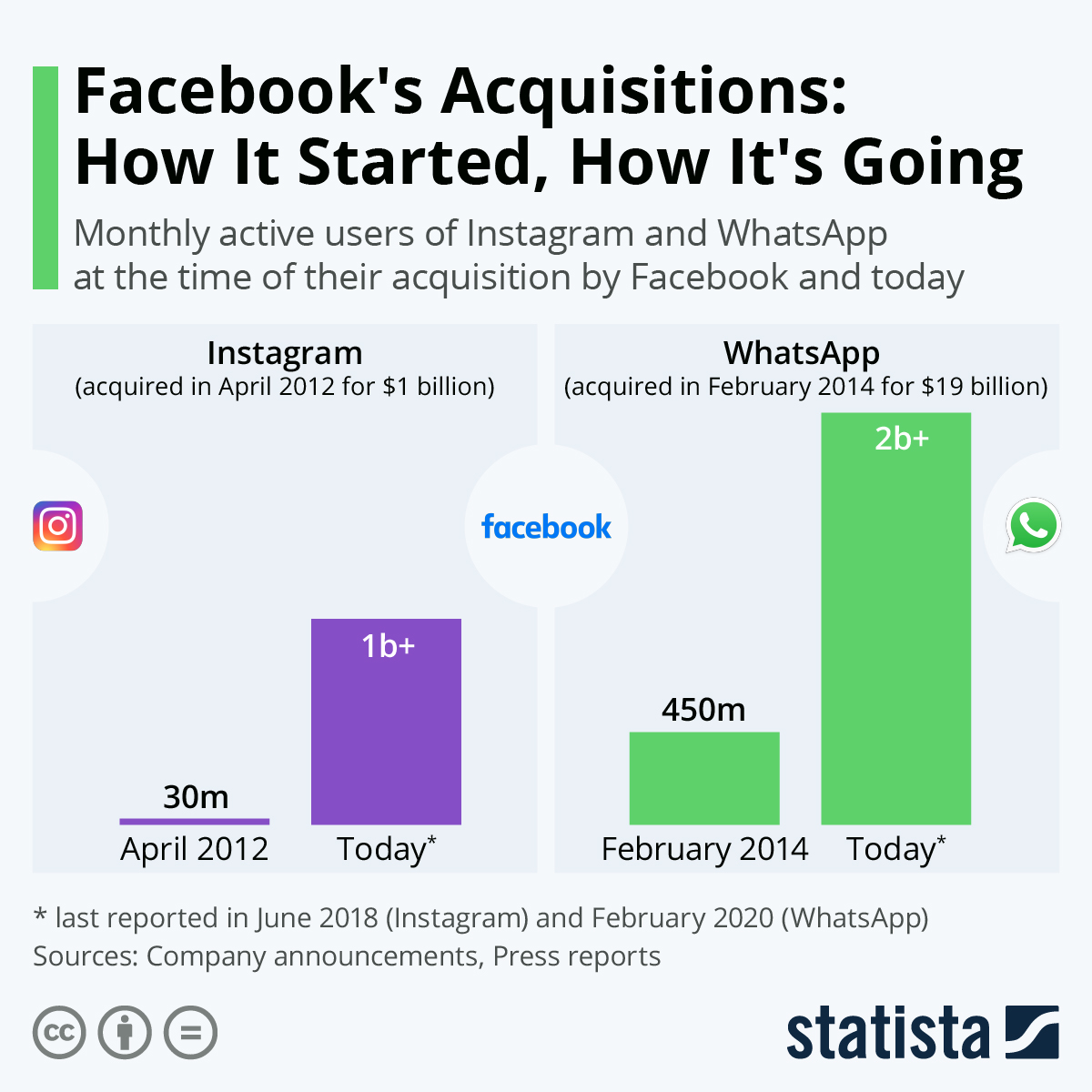

That changed the valuation conversation completely. The buyer was no longer thinking about paying a 5x or 10x multiple on our current revenue. They were thinking about what their stock price could do with that massive opportunity. This is why companies like Instagram and WhatsApp commanded what seemed like irrationally high valuations at the time of their acquisitions.

They weren’t being valued on their standalone performance but on what they would unlock for the acquirer.

A Dual-Track process can create huge leverage.

One of the best strategies for maximizing your exit value is running a dual-track process (meaning you’re exploring both a funding round and an acquisition at the same time).

This creates leverage in multiple ways:

- It forces acquirers to move quickly before a new funding round makes you more expensive.

- It makes investors more eager to commit, knowing that an acquisition is also on the table.

- It gives you options, so you’re never selling out of desperation.

A well-run dual-track process gives you more of an upper hand and puts everyone to work on your timeline.

It also provides a great answer when someone asks, “Why are you selling?” Instead of looking like a founder trying to exit at the first opportunity, you can say, “As CEO, my fiduciary duty is to explore all options to maximize shareholder value.”

M&A deals lose momentum fast.

Selling your company is like selling a house. If it sits on the market too long, buyers start wondering what’s wrong with it.

In M&A, time is not your friend.

At the start of an acquisition process, the power is on the seller’s side. There’s excitement, multiple bidders, and urgency. But the longer things drag on, the more leverage shifts to the buyer.

Once a term sheet is signed, exclusivity kicks in, and now a buyer will have more time to:

- Dig through financials and “discover” issues that can let them renegotiate the price.

- Add contingencies that weren’t in the original deal.

- Delay closing until market conditions become more favorable to them.

I’ve seen startups go bankrupt because an M&A deal took too long and killed their cash flow. Again, time is an enemy in an acquisition. Mark Zuckerberg once reportedly closed an entire deal over a weekend (incidentally, that deal was for Instagram). That’s the spirit of the ideal dynamic.

To have urgency and momentum on your side, keep these points in mind:

- Set a strict timeline for the deal. If it drags past that, move on.

- Use multiple bidders to create pressure and force fast decision-making.

- Avoid long exclusivity periods. Shorter exclusivity keeps your leverage intact.

There’s a whole other struggle after an exit

Most exit conversations focus on deal structure, valuation, and negotiation. What no one talks about is what happens after the exit.

Whether you stay at the company post-acquisition or move on, the shift is huge. You go from being the one making all the decisions to working within a larger machine. The cultural adjustment can be tough, especially if you’re locked into an earn-out period with financial incentives tied to your performance. That’s not even factoring in the possibility of acquisition indigestion (a topic for another post).

For those who leave, the challenge is different:

- You might experience identity loss after years of running your own company.

- Many exited founders struggle with a sense of purpose.

- You suddenly have financial freedom, but no clear next steps.

As Loom co-founder Vinay Hiremath famously (and boldly) declared: “ I am rich and have no idea what to do with my life.”

If I could speak to myself from 6 years ago, here’s the advice I would have given me before Vungle’s acquisition:

Set personal and professional goals before the deal closes. Don’t wait until after. Line up your next challenge, and realize it doesn’t have to be another huge hit. It could be as simple as spending more time with family or finally going on that vacation you’ve postponed 99X times.

And most importantly, you are much MORE than the company you built. There’s life beyond your first (or Nth) startup.

Closing thoughts

Exiting a startup is one of the biggest milestones in a founder’s life. But the best exits don’t happen by luck. They’re designed.

Your positioning prior to selling. The relationships you build before and during the exit process. How you balance timing and leverage. These are all critical factors that will hugely impact your outcome (although we don’t discount the many more elements at play beyond the ones I listed here).

Ultimately, the way you control the deal can have serious implications on whether you walk away with an average outcome, or something truly transformational.

P.S. None of this is meant as legal advice and is intended for informational purposes only. Always consult with professional advisors before finalizing any deal.

About the author

Zain Jaffer is a seasoned entrepreneur, investor, and the founder of Vungle, a mobile ad-tech platform that sold for $780M. Now a VC and real estate investor, he backs PropTech startups and shares hard-won insights on scaling, fundraising, and exits. Through Zain Ventures, he supports innovation in technology and real estate, and he is also actively exploring AI and its potential for streamlining workflows.