Founders are sometimes concerned that investors may steal their ideas. They usually come up with the same solution: "I will ask for an NDA before sending my deck."

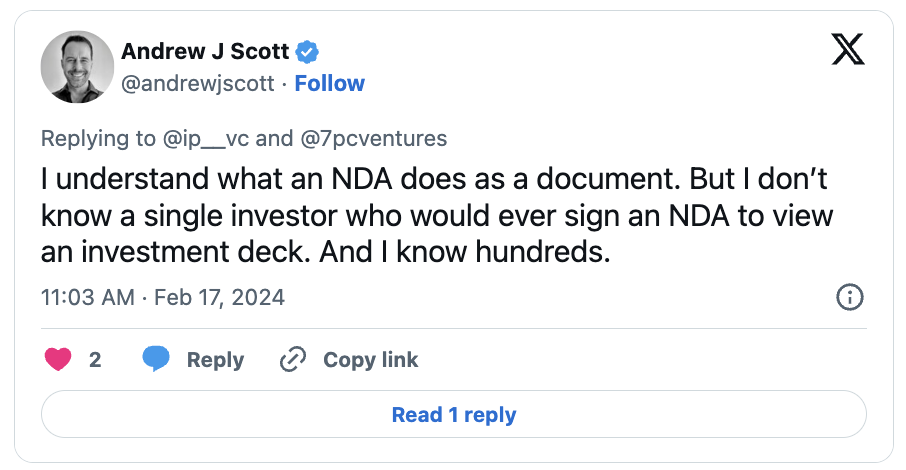

Yet, the NDA, or Non-Disclosure Agreement, is a document that no self-respecting investor will sign on first contact.

Today, I would like to explain why investors don't sign NDAs, and furthermore, why founders shouldn't ask for a NDA anyways.

Table of Contents

1. Founders don't have enough leverage to demand a NDA

That's the raw, simple answer.

For the investor, you’re just one of five pitches on a random Tuesday. They’ve got options. Why would they agree to an NDA?

Power dynamics are a thing, and in this case, they don't play in your favor.

2. An NDA adds unnecessary friction

Just like any sales process, less friction results in a higher conversion rate.

Especially with cold outreach, if an investor finds interest in your email, they should be able to instantly access the deck. Asking for a NDA first would absolutely crush your open rate.

On top of that, remember that investing is a social activity. Michael Haddad says it best:

3. NDA are for due diligence, not for first contact

Once the investor has confirmed interest, you will move to the due diligence stage, where sensitive information is shared: financials, IP, clients, etc.

At this point, you can probably ask for a NDA, and the investor has an actual reason to make the effort.

Before that, it's just too early.

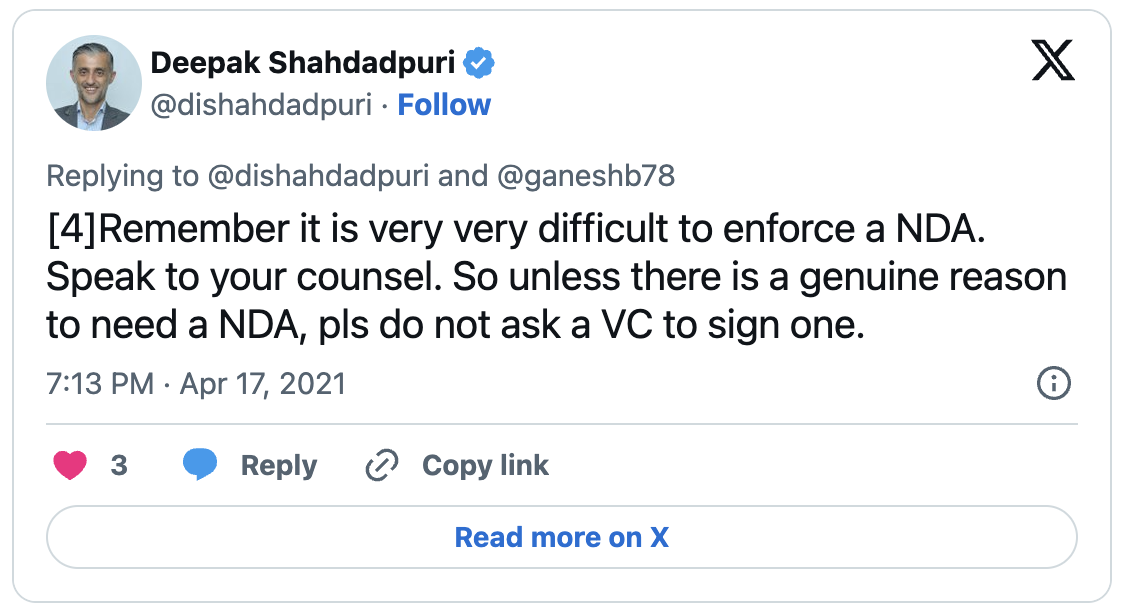

4. Founders cannot enforce NDAs anyways

Do you have $100k to spend in legal fees anyways? Probably not.

So what will you do in the unlikely case where the VC breaks the NDA? Probably not much.

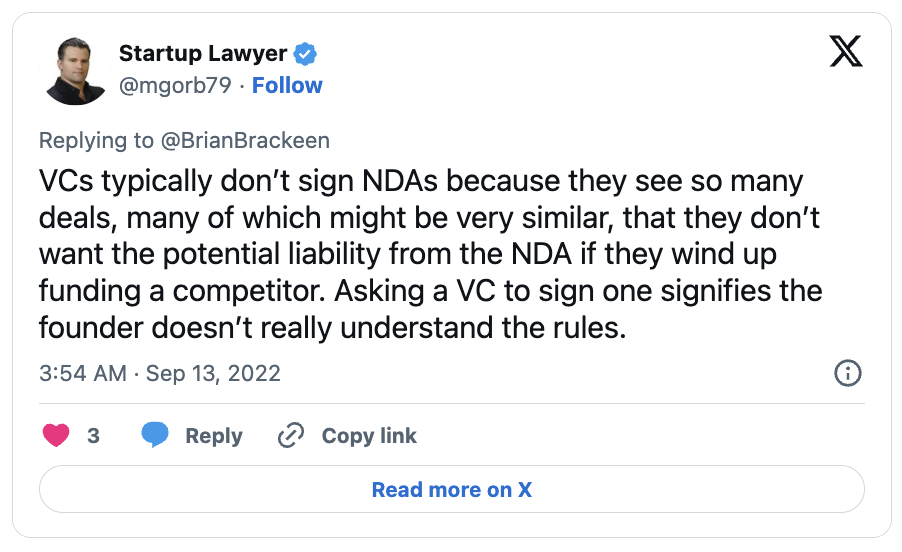

5. Signing NDAs would put an absurd legal weight on the VC

A VC reviews hundreds of pitches for companies that are similar to yours. That's the definition of their jobs.

Signing a NDA with every company they meet would put an absurd legal weight above their heads. Maybe they could do it for 1 company. For 100, there's no way. It's just not realistic.

6. Asking for a NDA has become a negative meme in itself

For all the reasons listed above, asking for a NDA is not the industry standard.

By asking for an NDA, you're signaling that you don't know any better. You're signaling that you're an outsider, a noob founder who probably values idea over execution.

For many investors, that signal is enough in and of itself to be a deal breaker, regardless of the merits of your startup.

Here's how to protect your startup without a NDA

The truth is there's not much you can do to protect your startup while raising funds.

Still, here are 3 things you could do:

- Keep the confidential information outside of your deck. Even if you're building deeptech or biotech, you don't need to share details about your IP in the intro deck. A high-level view is usually enough to validate interest and get a first call. As a general rule, always assume that your intro deck will be read by your main competitor and act accordingly.

- Research investors before sharing too much. Before meeting with an investor, research their portfolio. Did they recently invest in a direct competitor? If yes, you may want to skip the meeting.

- Have a killer team with a strong ability to execute. The best safety measure is to be desirable. Make people want to invest in you rather than compete with you. And if they do steal your idea, you can still out-execute them.

At the end of the day, "ideas are just a multiplier of execution". (Derek Sivers)

Your idea may be good, but it's only valuable if you can execute - and it's pretty much worthless otherwise.

To protect your idea, you may choose to go stealth, but this will hinder your ability to raise, and more broadly, your ability to execute.

Sure, there are exceptions, but the trade-off is probably not worth it.

Find your ideal investors now 🚀

Browse 10,000+ investors, share your pitch deck, and manage replies - all for free.

Get Started

![12 Best Startup Financial Model Templates [Free & Paid]](https://d1pnnwteuly8z3.cloudfront.net/images/177302d9-3657-45b7-ac9d-acf801d83a74/019fadd2-2388-77a4-a43e-6c44f536d546.jpg)