The financial landscape from 2020 to mid-2022 was marked by a considerable surge in equity fundraising deals, both in value and volume, from the seed phase all the way through to series B and C. Thanks to the enthusiasm for the tech sector in general during this period, as well as ample liquidity on the market, valuations soared.

Presently, some of these companies are contemplating further transactions, whether a new fundraising round or a sale. With the market experiencing a sharp slowdown, many of these companies have to deal with a dark spot in their equity story: a lower valuation than the previous round. In this article, we look at how to deal with this delicate situation.

Table of Contents

1. Studying waterfall and its implications

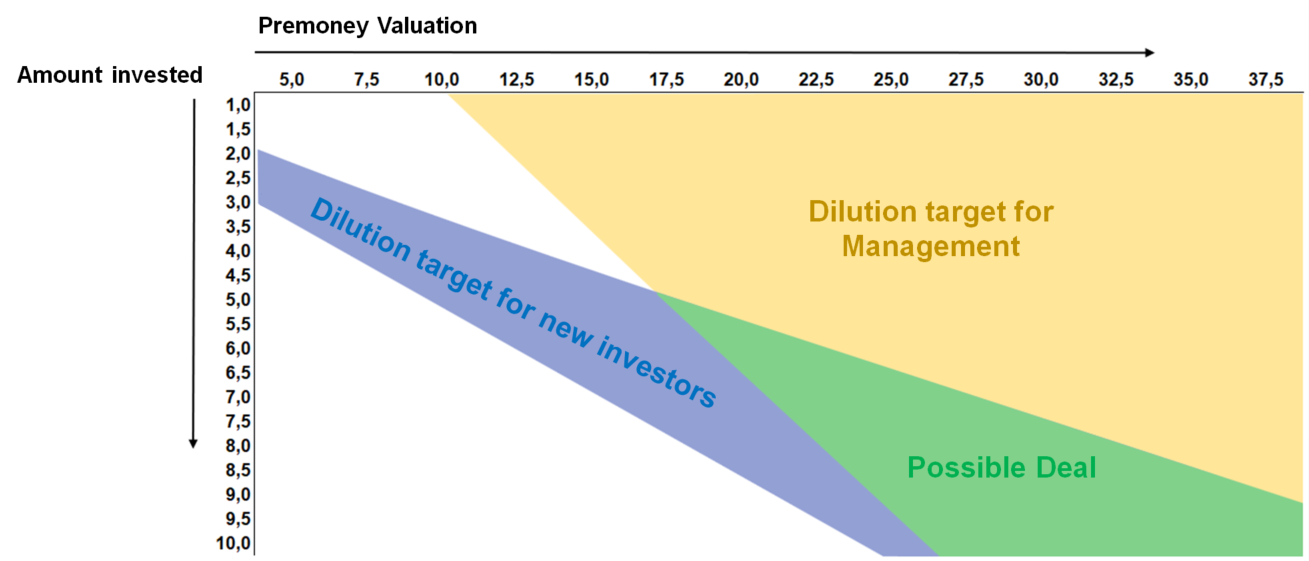

The "waterfall" refers to the way all cash is distributed in the event of the sale of all or part of a company's shares. It is essential to understand how this allocation is structured, and to assess potential risks, in particular by pointing out possible misalignments. Excessive valuation can reduce the incentive for certain stakeholders to contribute to the company's success.

For example: a three-founder team raised $4m in a financing round at a pre-money valuation of $16m. The company has a net debt of $4m. Investors benefit from a preferential liquidation clause and an anti-dilution clause ("ratchets"). 18 months later, the market has turned. Valuation, once a source of pride, has become a burden.

1.1 The case of a fundraising

A new fundraising round based on a lower valuation is complicated: investors would trigger the anti-dilution clause, and this would sharply reduce the level of ownership of the founders and business angels. New investors will not be thrilled...

If the management is to hold more than 50% after exercising the anti-dilution clause*, and the new investor wishes to hold 20 to 30%, it is mathematically impossible to make a round with a lower valuation than the previous round.

* For the purposes of this example, we have taken a full-ratchet clause out of the various possible wordings, which mainly benefits investors.

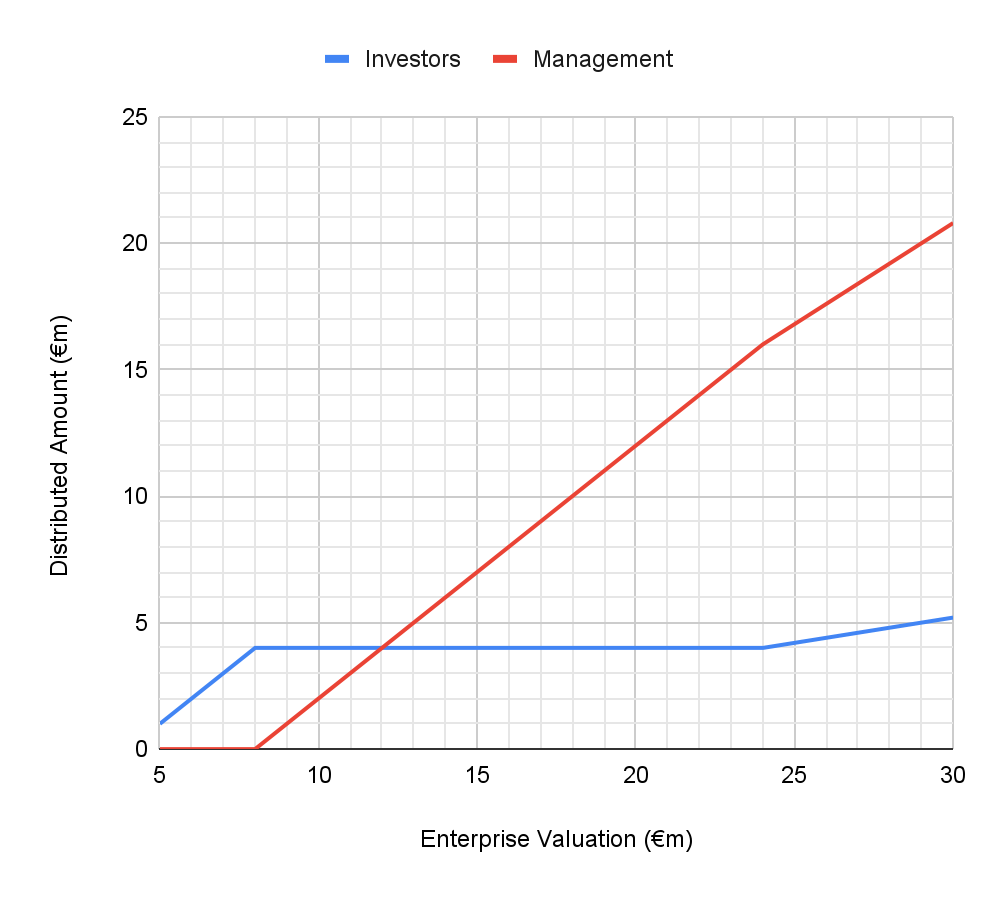

1.2 The case of a buy-out

A buy-out with a valuation of less than $8m would not return any money to the founders: they would have to reckon with $4m of remaining debt, and $4m redistributed preferentially to investors. Years of hard work for nothing. Below this valuation, from the founders' point of view, they might as well go bankrupt...

Despite an 80% shareholding, the founders receive nothing if the sale takes place at a company valuation of $8m or less, while the investors have no marginal gain between an exit at $8M and an exit at $24m (!) The alignment of stakeholders is therefore far from optimal.

2. Communicating with stakeholders

Communication with co-founders, the board of directors and shareholders is crucial to identify the problem and assess everyone's commitment to solving it.

If the discrepancy between the financial conditions of some and the company's situation is too great, it will be necessary to renegotiate internally before embarking on any new operations.

A number of concrete actions can be contemplated:

- The most classic solution is to set up a stock option plan to increase the founders' stake in the company, linked for example to the achievement of targets.

- Difficult and rare, but sometimes necessary, is the renegotiation of preferential liquidation and anti-dilution clauses. In the most extreme cases, this means transforming preference shares into ordinary shares.

- In the case of a buyout, it is not uncommon for investors to motivate founders to complete the sale despite the presence of a preferential liquidation clause, for example by means of a bonus in case of success. This bonus could, for example, be linked to the achievement of a certain price per share.

Each situation is unique, but in all cases, high-quality relations between the co-shareholders are key to ensure that these discussions proceed smoothly, despite numerous external pressures and uncertainties.

3. Preparing for a new financial operation

Even in the case of a small operation, it's important to be up to date with rapidly changing market expectations. The appropriateness of a new operation has to be judged in the current context.

Passively waiting for better days in terms of valuation is an option, but the risk must be carefully weighed. The period from 2021 to 2022 was marked by a valuation peak, but it is also possible that the situation deteriorates further and never returns to these levels.

In the event of a green light to launch a new round of fundraising, new investors should be made aware of the internal work carried out to maintain the alignment of the stakeholders of which they will be a part.

The consequences of such action will generally be less significant in the context of a buy-out, but no acquirer will willingly enter a madhouse, even for the duration of a negotiation: the risk of never seeing existing shareholders come into agreement is a real one.

Last but not least, you may find it useful to call on the services of a professional investment bank, especially if you lack the necessary perspective on your situation and the options open to you.

About the author

Augustin de Cambourg is a co-founder at Raisers Partners where he provides fundraising and M&A advisory services to innovative companies from late-seed to series C. Deeptech, mobility, and healthcare are his main industry focus. Augustin and his team have transacted for over €245m across 50+ deals in the past few years. More information on raiserspartners.com.

Find your ideal investors now 🚀

Browse 10,000+ investors, share your pitch deck, and manage replies - all for free.

Get Started

![12 Best Startup Financial Model Templates [Free & Paid]](https://d1pnnwteuly8z3.cloudfront.net/images/177302d9-3657-45b7-ac9d-acf801d83a74/019fadd2-2388-77a4-a43e-6c44f536d546.jpg)