Have you ever wondered how a VC can review 20 decks per day and still be on time for padel at 5pm?

That's because of “signals”, of course.

Signals are small hints that investors use to make a quick decision about your company. No need to sit down with you, no need to listen to your vision… Two minutes with your deck, and your fate is sealed: you get rejected or you get a meeting.

That's why founders should care about VC signaling.

Understanding your signals will not only increase your chances to get funded, it may also help you flag and fix issues in your business.

Without further ado, let's jump into the hellhole of VC signaling.

Table of Contents

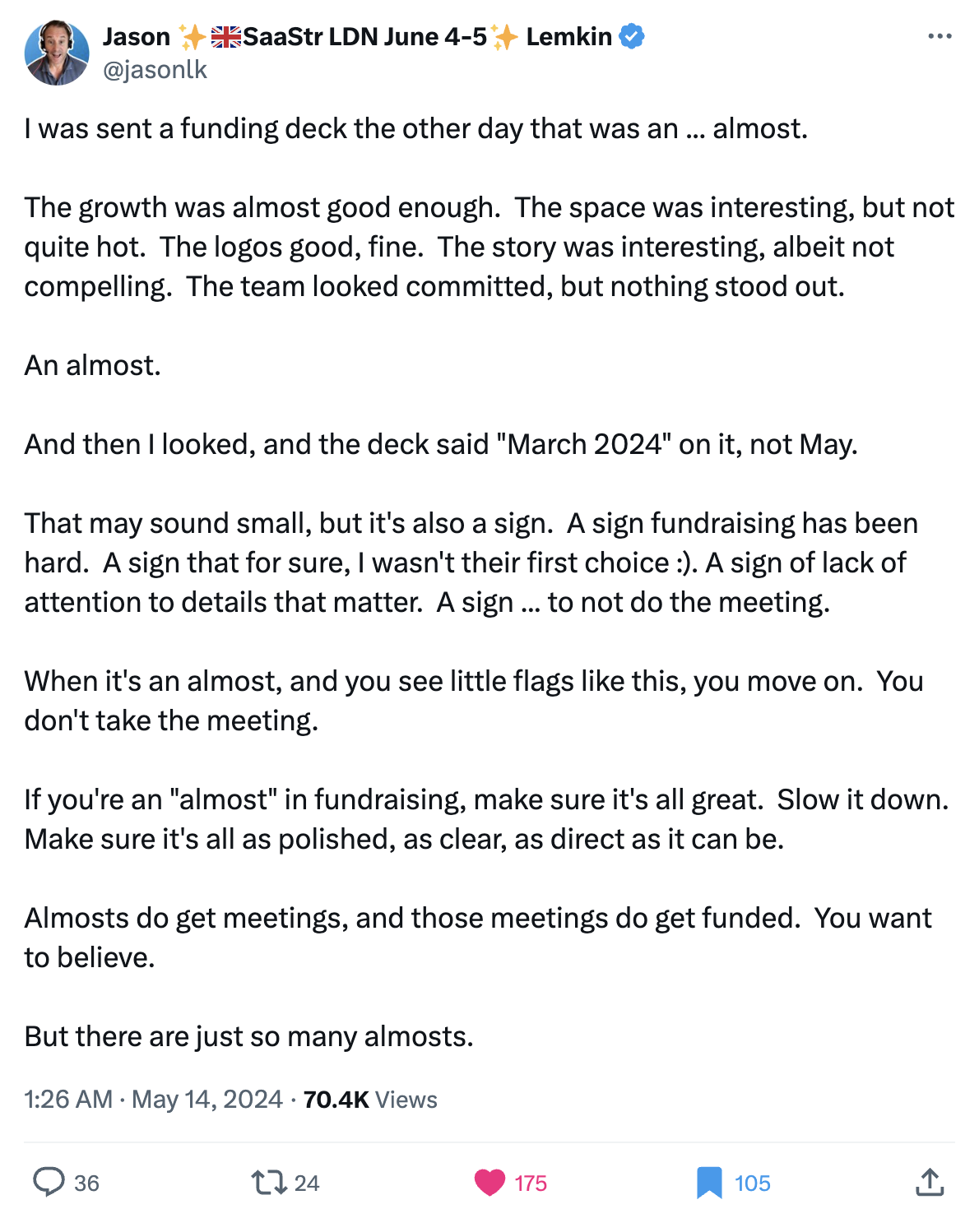

1. The date on your cover slide is outdated

You think I'm kidding, but I'm not.

When your deck cover says “March” and it's May, you're telling investors that you have low attention to details. Worse, you're signaling that you've been raising for 2 months and still on the hunt.

Here's what renowned VC Jason Lemkin had to say about it:

(I broke down this story in my post VCs aren't your friends.)

Even assuming you keep your cover updated, your old deck will still circulate behind your back and reveal the actual date you started raising. You don't want that.

The solution?

Just don't put a date on your cover. That's the smart thing to do.

2. Your SAM is larger than $100B USD

When a founder claims a $100B+ market, their market sizing is usually too broad and therefore, the maths is wrong.

Let's say you're building a mobile app for personal budgeting. Your market size is NOT $935B (global spending on mobile apps in 2023 according to Statista).

You have to narrow it down:

- Is your app available in China? Then remove all Chinese consumers.

- Is your app sold to professionals? Then remove the B2B segment from your market size.

- Is your app relevant to people who don't budget? Then that's another chunk you take away from your market size.

- Etc etc.

If you slap a humongous market size on your deck, you better back it up well.

3. “If we just capture 1% of the market…”

There's nothing wrong with the sentence in itself, but it's been overused by founders dreaming aloud in front of investors, so it's become a red flag.

You're better off not saying it.

4. Your SAM is smaller than $1B

The “SAM” or “Serviceable Addressable Market” is the market suze that investors care about. As a startup, you're supposed to capture a portion of that SAM within 7-10 years, and this portion times a multiple will determine your exit valuation.

Now, let's do some basic VC maths.

Long story short: show VCs that your market is large enough to support a VC-friendly exit.

This means a SAM above $1B.

5. You make empty claims

When communicating with investors, be specific.

A common mistake consists in making big claims about your team, traction, or tech, but not supporting them with facts.

This is a problem because many wannabe founders are total bullshitters. You don't want to be one of them. So when communicating with investors, always back up your claims with facts, names, and numbers.

6. You ask for a NDA before sending your deck

This is a classic signal for “I have no idea what I'm doing”.

Founders are sometimes concerned that investors may steal their ideas. They usually come up with the same solution: "I will ask for an NDA before sending my deck."

Yet, the NDA, or Non-Disclosure Agreement, is a document that no self-respecting investor will sign on first contact. I deep dive on the reasons in this post Why VCs won't sign your NDA.

In short, a NDA may be warranted when you reach the due diligence stage. Before that, you will look like the infamous meme.

7. ‘We have no competition”

This one is another “instant death sentence”.

It is virtually impossible for a startup to have no competition.

Instead, you probably have two dead angles:

- Other teams are building similar tech, and you're not aware of it. For example, a Chinese team is also building a car engine that runs on water, and you just don't know about it.

- Other products are solving the same problem with a different solution. For example, a petrol engine, an electric engine, a horse, would all be competitors to your water-powered engine as they all solve the same problem - make the car go vroom!

If you don't want to sound silly, get a good grasp of your competitive landscape - not just the tech, but the overall value proposition.

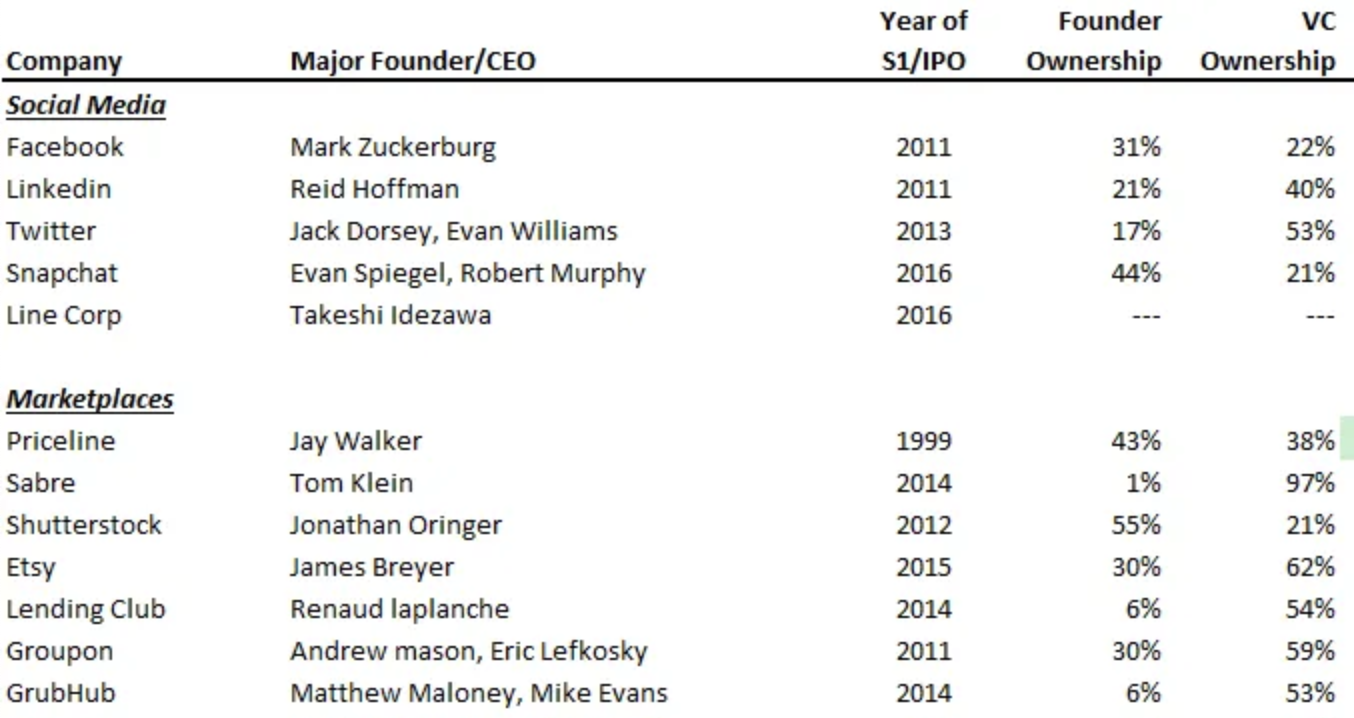

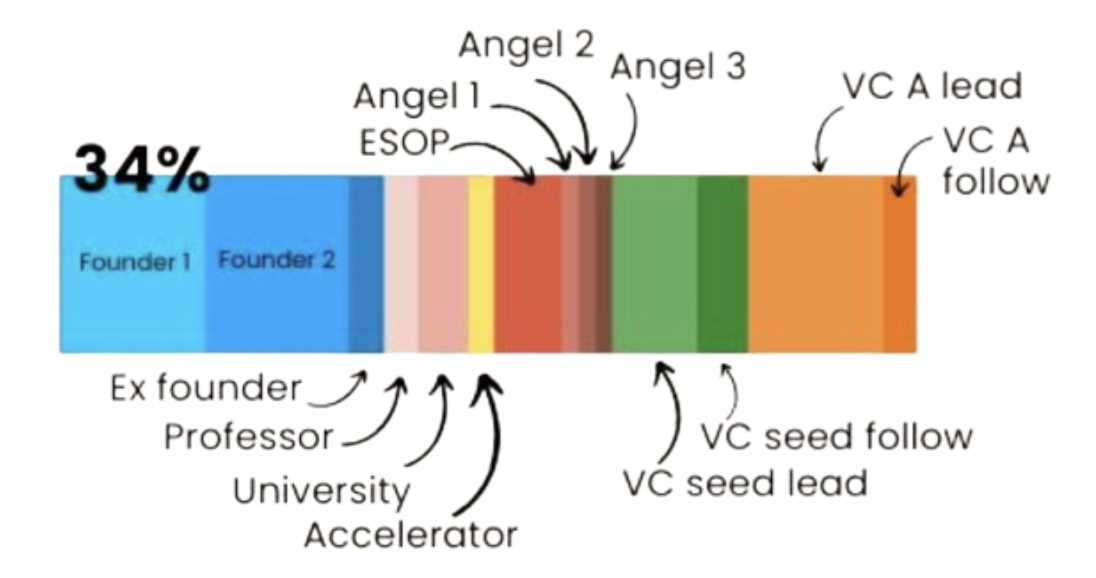

8. The cofounders own less than 50% after Series A

It is generally admitted that the founders should collectively own 50%+ of the cap table after Series A in order to be sufficiently incentivized. This means owning at least 70% after seed.

If you own less than that, some VCs may see this as a red flag and pass.

For reference, here's how much equity successful founders owned at IPO, courtesy of Blossom Street Ventures.

And yes, Hubspot sold 47% of their cap table at Series A. It was back in 2007.

It's 2025, people. We don't do that anymore.

9. You have dead equity on the cap table

The early days can be messy for your cap table.

Here are some of the horror stories you might encounter:

- A university (probably British…) owns 30% of the cap table because part of your tech was born in their labs

- A cofounder leaves right after year 2 with 25% of the company

- An “angel” investor gave you the $50k you desperately needed - for a 30% stake

- A startup studio owns 50%+ of the company at pre-seed

- A greedy advisor somehow ended up with 5% of the cap table

As a consequence, you're unlikely to be able to retain enough ownership for yourself. You will also struggle incentivizing the employees you need. And finally, you're signaling poor judgement and decision making skills.

And look, I'm not blaming the founders here. Every startup has a different origin story. You gotta do what you gotta do to get things off the ground.

But when it's time to raise, investors don't care about the “why”.

They just see a broken cap table. A millefeuille.

10. Your market size is expressed in volumes rather than value

It's a small detail, but when discussing market size, you want to express it in value: USD, EUR, etc.

Of course, you should know the underlying volume assumptions.

But what everyone really cares about is the $ value.

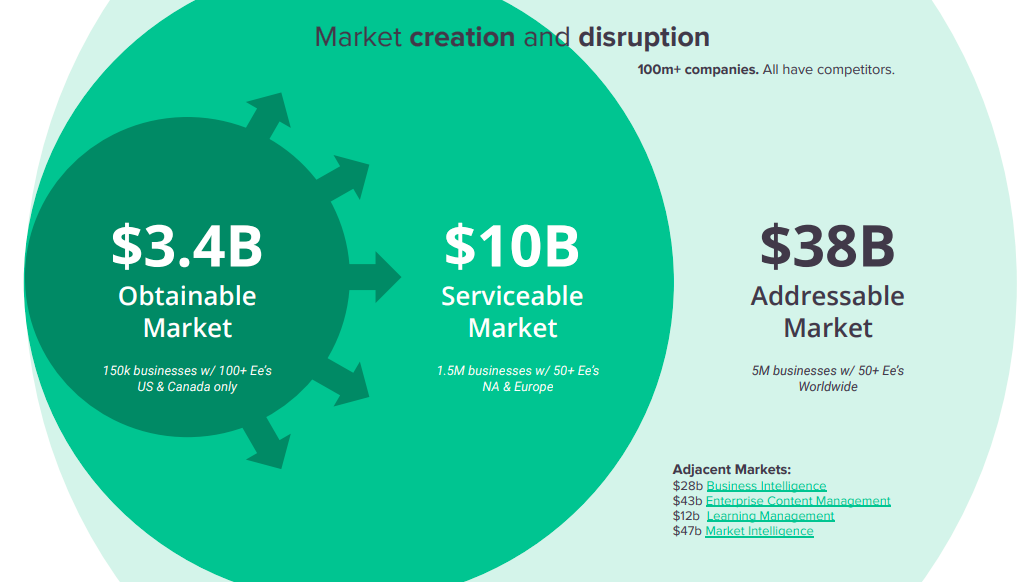

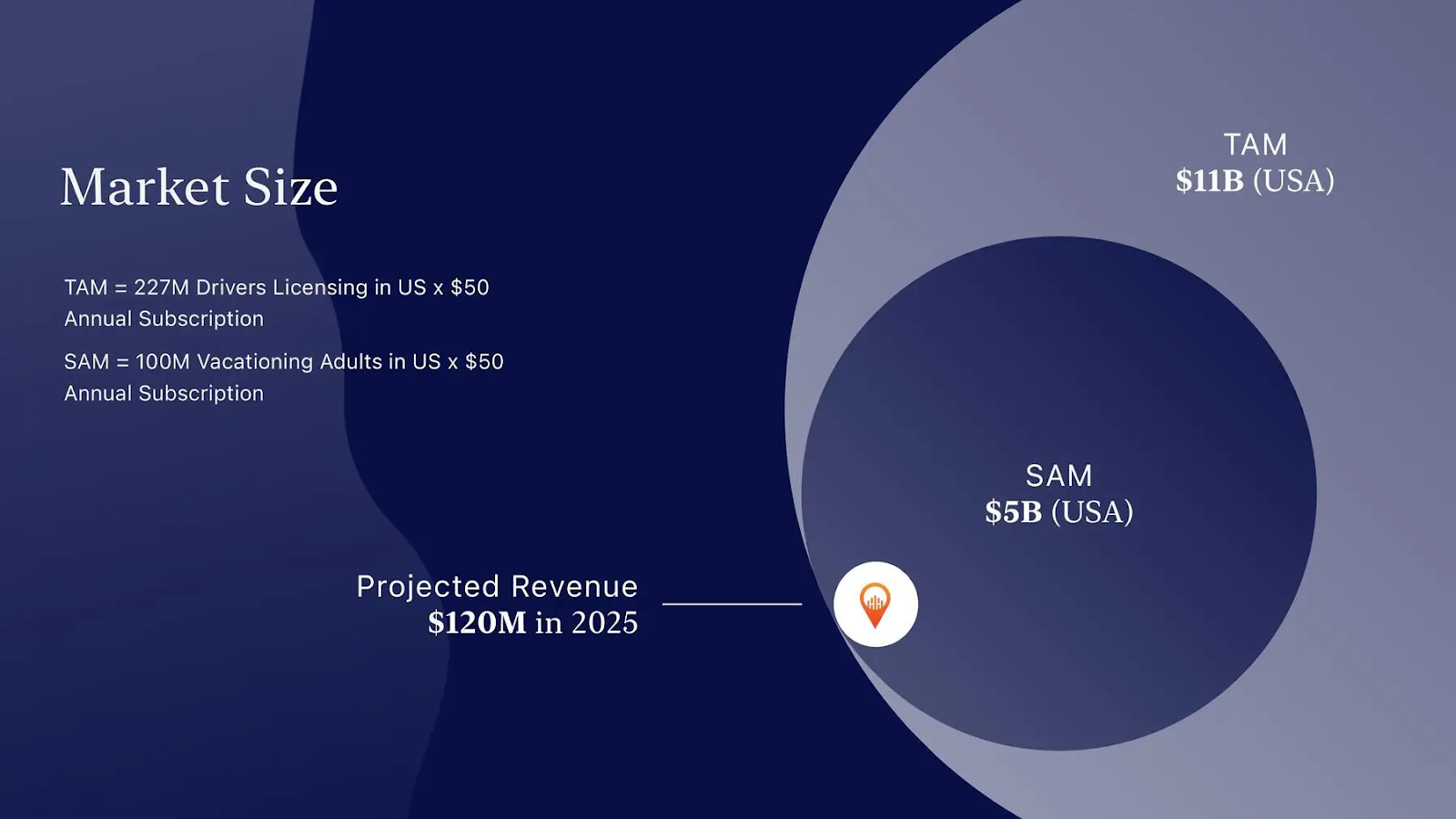

11. Your market sizing is top-down rather than bottom-up

There are two ways to calculate your market size:

- Top-down: You just grab a number from whatever online market research

- Bottom-up: You multiply the ARPA by the # of clients in your market

The bottom-up approach is preferred by investors because you have control over the underlying assumptions. You can't pull the number out of thin air, you must have done your homework.

So when discussing market sizing, display a bottom-up approach.

Here's another example of a good market sizing

12. You're not a Delaware C-Corp (or a VC-friendly legal entity)

If you're talking with American VCs, they almost always only invest in Delaware C-Corp.

If you're raising in Germany, France, China.., there is a form of legal entity preferred by VCs for each jurisdiction.

There are reasons for that, mostly taxes and jurisprudence. And yes, you may have started as an LLC. But make sure you flip to the VC-friendly entity BEFORE engaging conversations. Otherwise, it's yet another negative signal that you're just not investable yet.

“Looks cool, come back when you have a C-Corp”

13. You have no chef in the kitchen

A restaurant needs a chef. A plane needs a pilot. A tech startup needs a tech lead.

No investor will seriously consider investing in a tech company that doesn't have a tech lead in place.

Actually, most VCs prefer when the tech lead is one of the founders. It's a strategic role, and you want someone fully committed to the company.

So no CTO = 90% red flag

14. Your pitch deck is ugly

You know how founders obsess about their homepage: they iterate on the design and UX, refine the fund, adjust the copywriting, measure bounce rate, etc.

Well, your deck plays the same role for investors. Your deck is the landing page of your raise.

For your own sake, make sure it's not too ugly. Font, palette, alignment, text density… Just give it a bit of love. Get a template or a designer if you need help.

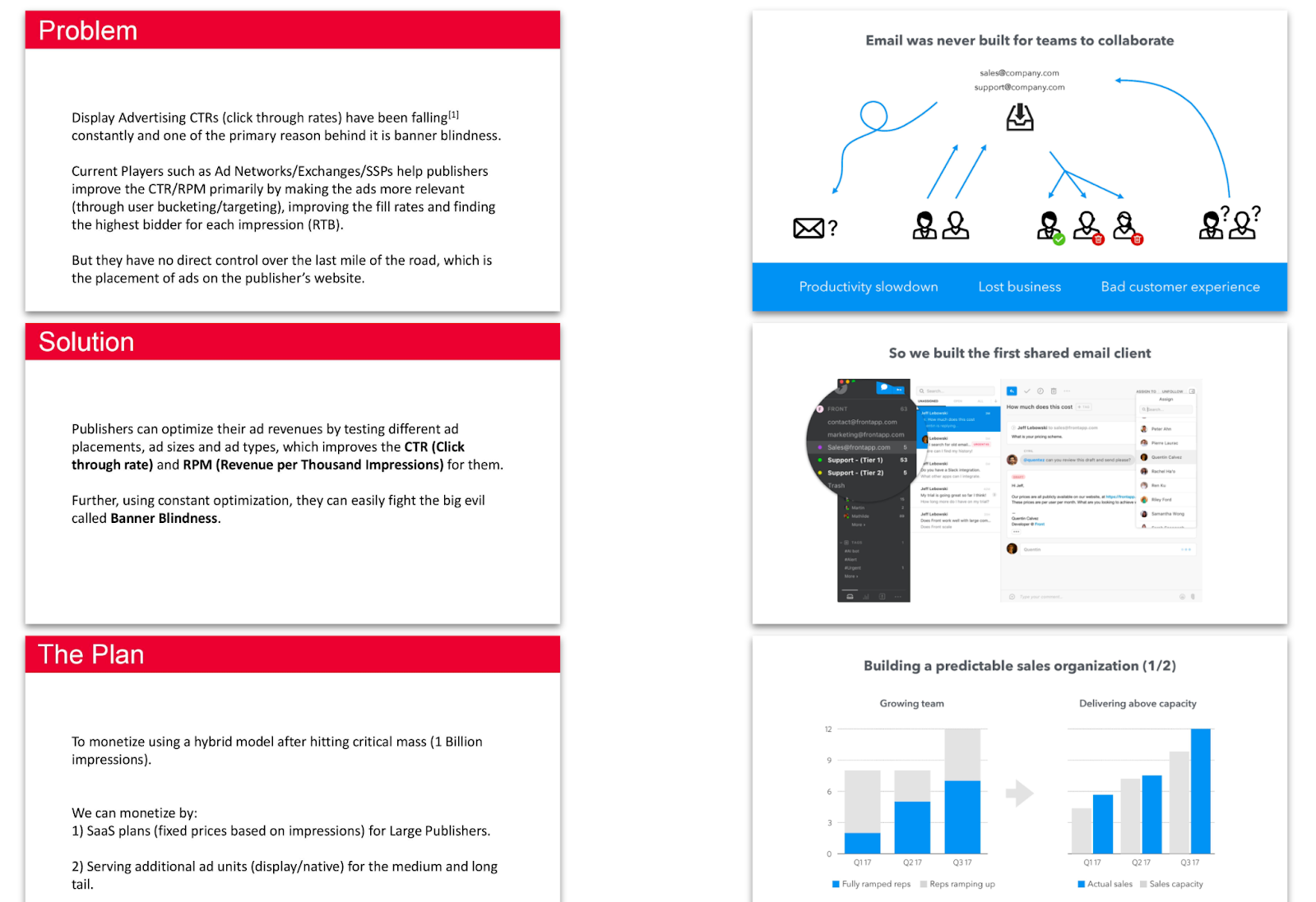

Come on, let's be honest. Would you rather read the deck on the left or the right?

15. Your want to sell to everyone

This is another sign of an inexperienced founder: he or she wants to sell to everyone.

“Our product is amazing. It will sell to men and women, young and old, all around the world. Our market is everyone”.

Veteran founders know it's not true. You can't be the best at everything, especially not in the early days when resources are scarce and you need to focus your efforts.

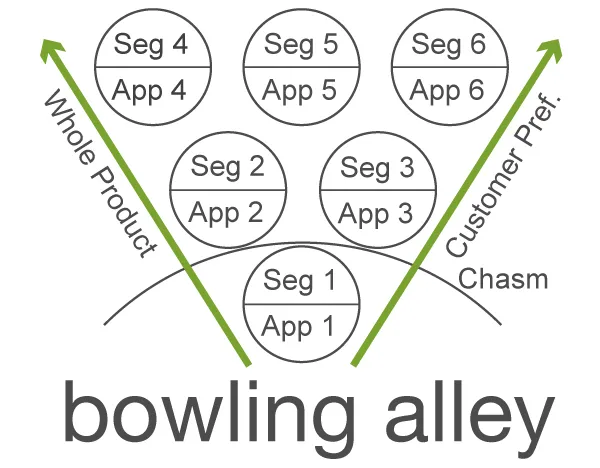

Instead, you should “start small and think big”.

Identify a beachhead i.e. the intersection of a relevant segment and application. Dominate it, then expand methodically following the “Bowling alley” model developed by Geoffrey Moore in “Crossing the Chasm”.

This is what investors expect, and what has proven to work repeatedly.

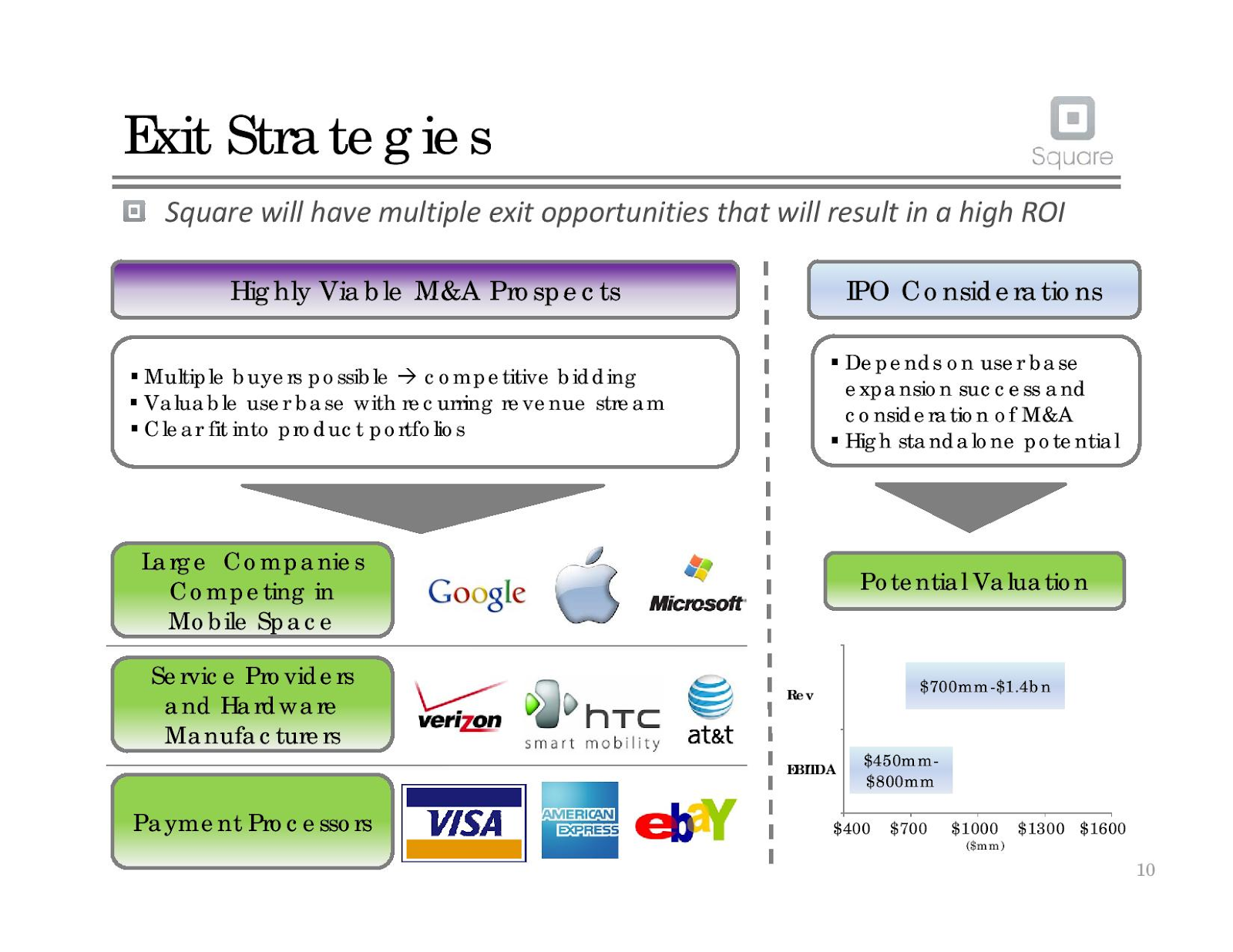

16. You talk about exits too much and too early

Talking about exits when you're raising pre-seed is a premature conversation. You should be worrying about getting to PMF instead.

Founders obsessing early about exits can be a red flag for investors.

There are really only two cases where it's ok to have an “Exit” slide in your deck.

- You're building with the explicit purpose of a strategic acquisition. Typically, you already know who the buyer will be, you already have connections there, and it's almost an insider play.

- Your founding team has had previous successful exits, so you know what you're talking about. You're not going to sound like a delusional dreamer.

See the slides below. Square had an Exit slide, but they also had the CEO to back it up. And it was a Series C.

17. You use jargon like “disruption” or “transformation”

Investors are allergic to jargon.

You may think jargon sounds smart, but the room is full of smart people, and you're not going to impress anyone. Quite the opposite actually - you will annoy the hell out of whoever is still listening to you.

Paul Graham has championed “ speaking simply ” for startups and VCs, and it has gradually become the norm in the industry.

So keep it simple.

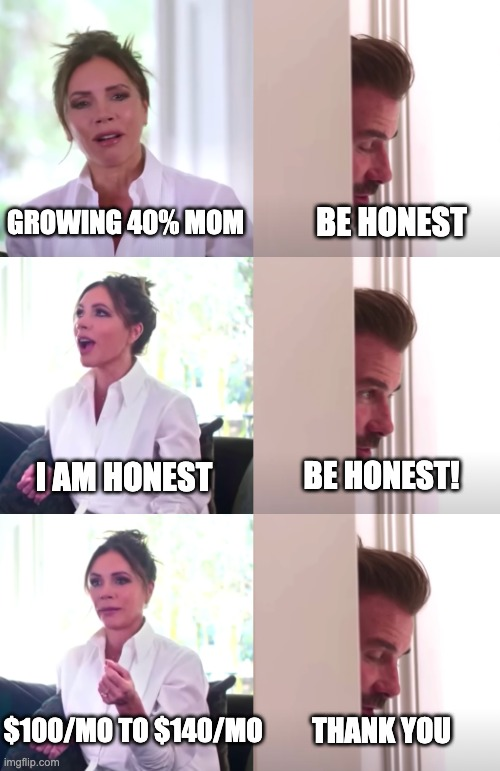

18. You misrepresent your traction or track record

Sometimes, I get emails from founders claiming “a previous 8 figure exit” or “revenue growing 40% MoM”. Nice!

Then we get on a call. It turns out that the founder was a junior at that company that exited, not the CEO. And that revenue growth? Yes, revenue grew… from $100/mo to $140/mo.

You wasted my time, and in the process, you nuked your credibility.

Don't mislead investors to get a meeting. Your name is your most precious asset.

19. You're using a gmail/hotmail address

Small signal, but not trivial.

If you're serious about your startup, get a custom business email address to communicate with investors (but also clients, partners, etc).

It costs $6/mo with Google Workspace, and you're set.

The only exception is founders using their MIT or Stanford email address to signal their track record to investors.

Other than that… drop [email protected] and get a custom email address.

20. Your LinkedIn profile is still showing you old job

Classic mistake.

You're at an early stage and not paying yourselves. Therefore, your team might be working on the side, either at a day job or doing some freelance work. That's legitimate.

However, this may worry some investors.

Once you raise, investors will expect you to go full time. If your profile still shows you or your cofounders at your old job, they might be concerned. Is this stellar CTO truly on board and committed? Or is it just a front to raise capital?

At the very least, you should have your occupation at the startup listed at the top of your Linkedin profile.

And do the same with every key person in your team.

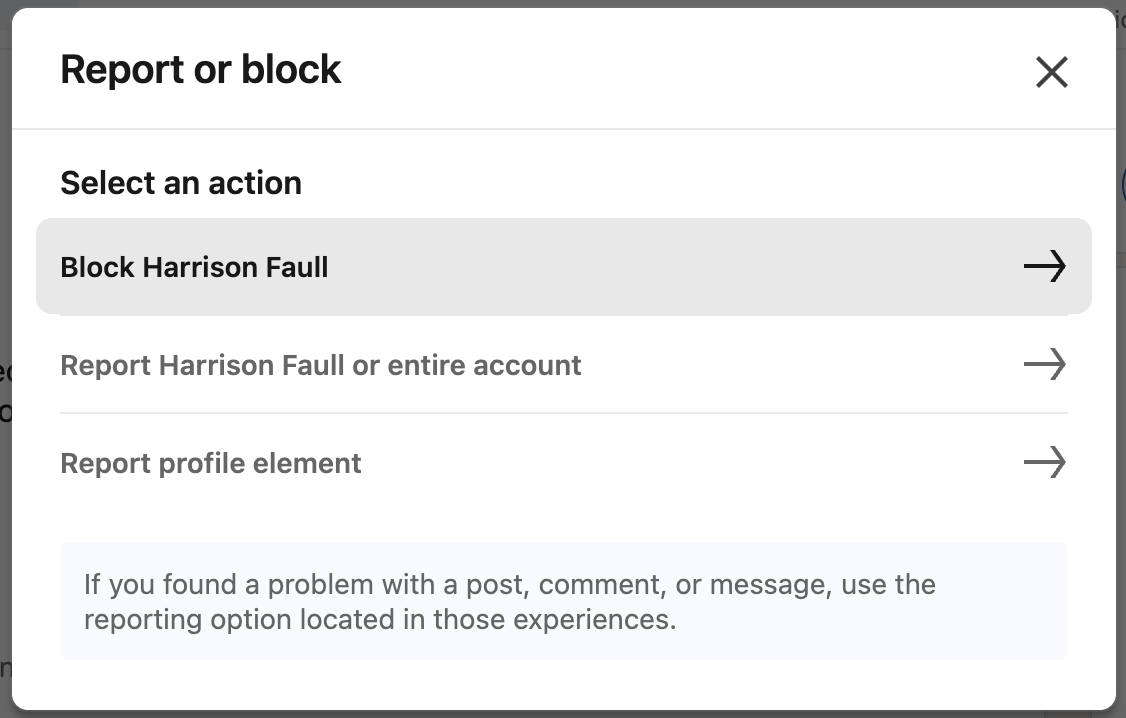

Pro tip: you can hide your LinkedIn profile from your boss and colleagues by going to their profile, clicking “More”, then “Report or block”, and “Block”.

21. You cannot make educated guesses on CAC/LTV

Up to Series A, you rarely have solid numbers. Nobody expects you to know your customer acquisition costs (CAC) or your customer lifetime value (LTV) at pre-seed, and rightfully so.

It doesn't mean you should be completely ignorant, though.

CAC and LTV are critical to your business model. Any self-respecting investor expects you to have “an educated guess”, meaning that you looked up industry standards, competitor numbers, modeled out a couple of channels, etc.

A case in point would be dating apps. Dating apps live and die by their CAC and LTV. Your product is almost secondary - it's all about your growth and retention. Even at the pre-product stage, if you cannot hold a credible conversation on these topics, most investors would be alarmed.

Obsessing about distribution is a mark of experience.

22. You're not sending the CEO for VC conversations

In the early days, the CEO is the person in charge of raising.

When getting on a first call with the company, investors expect to talk to the CEO. Not the CTO. Not the CFO. Not the COO. Not the fundraising advisor. Not the executive assistant.

The CEO.

Sure, you can have people supporting your raise in the background, helping with list building, deck design, outreach campaigns...

But the CEO should be the public front of the operation.

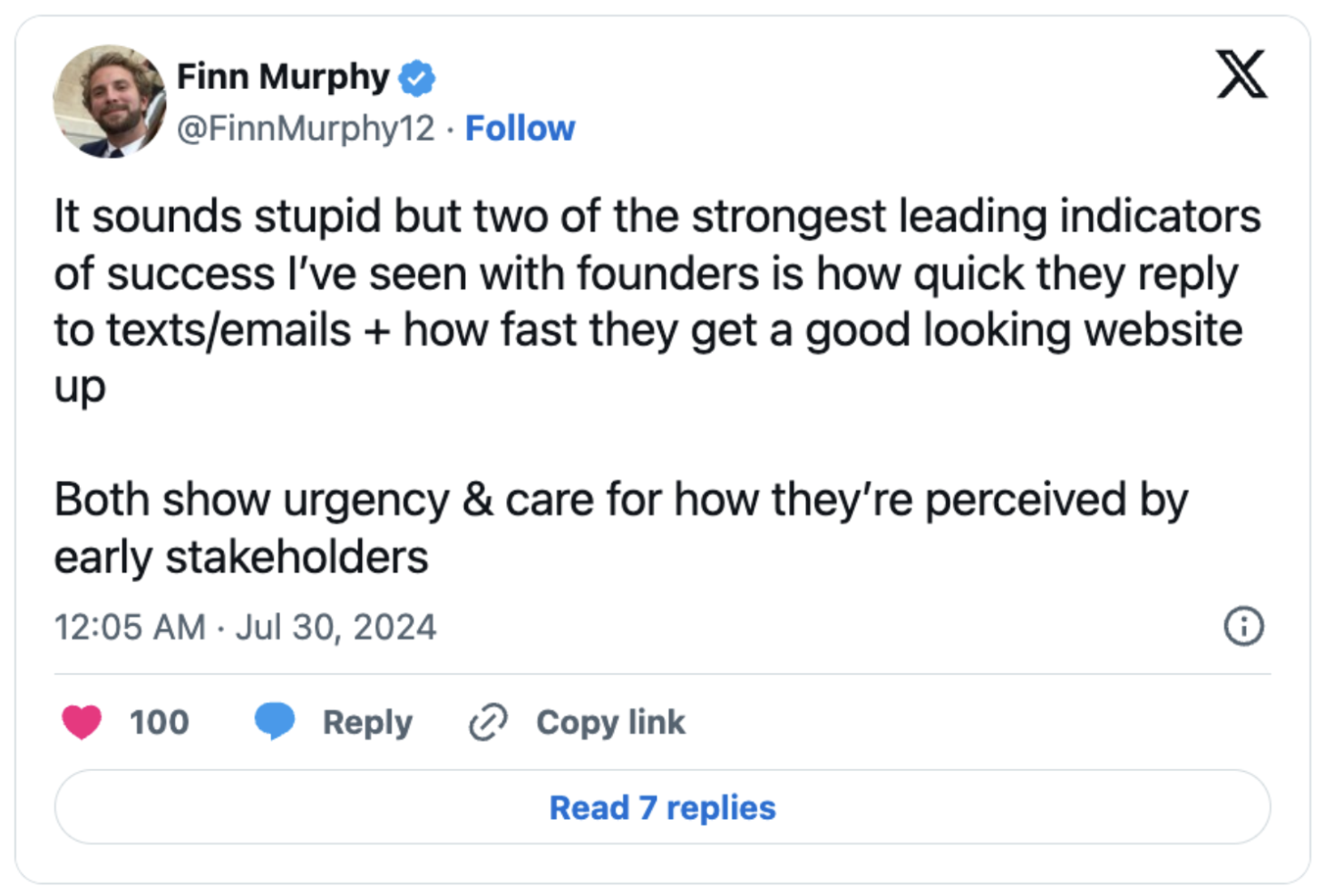

23. You're slow to reply to emails

Founders who reply fast to text/emails are perceived as more likely to succeed.

You'll hear that from a lot from VCs.

Therefore, founders who are slow to reply are perceived… less likely to succeed.

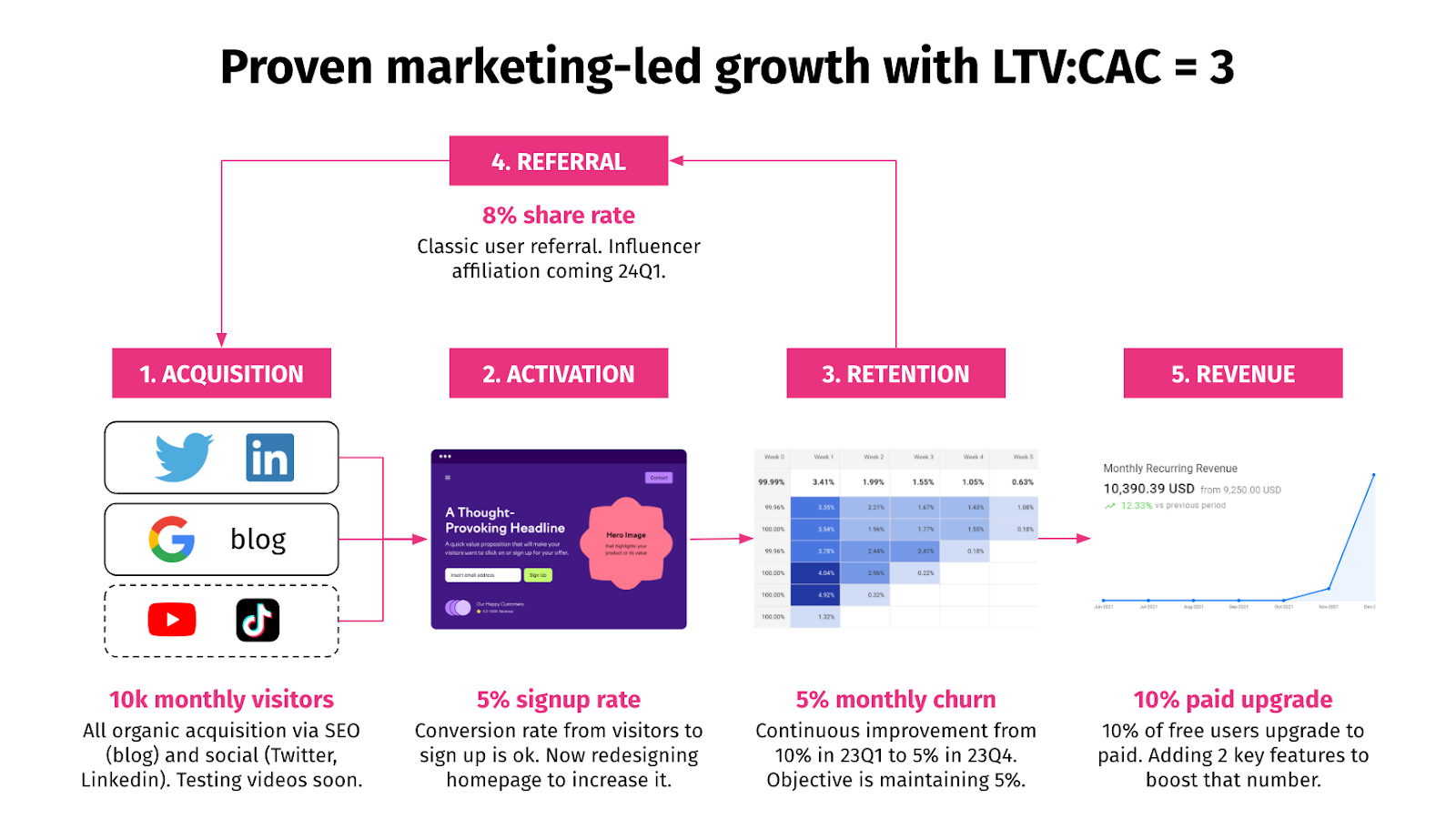

24. Your GTM strategy is a laundry list of channels

When asked about go-to-market, many founders will just throw around a list of channels.

“We'll do SEO, and social media, and partnerships with influencers. We'll also go to events and conferences. Oh, and we will also do cold email outreach. Mmhh… And yes, we will also pay for ads on Google and Facebook. And some billboards everywhere.”

This shows poor understanding of your market. It's unlikely that your target clients are receptive to all of the above.

It also shows poor prioritization. Even after a seed round, you rarely have the resources to test, learn, and scale 10 channels in parallel.

Instead, investors expect to see a couple of relevant channels feeding a well-designed conversion funnel, with some key metrics at each step.

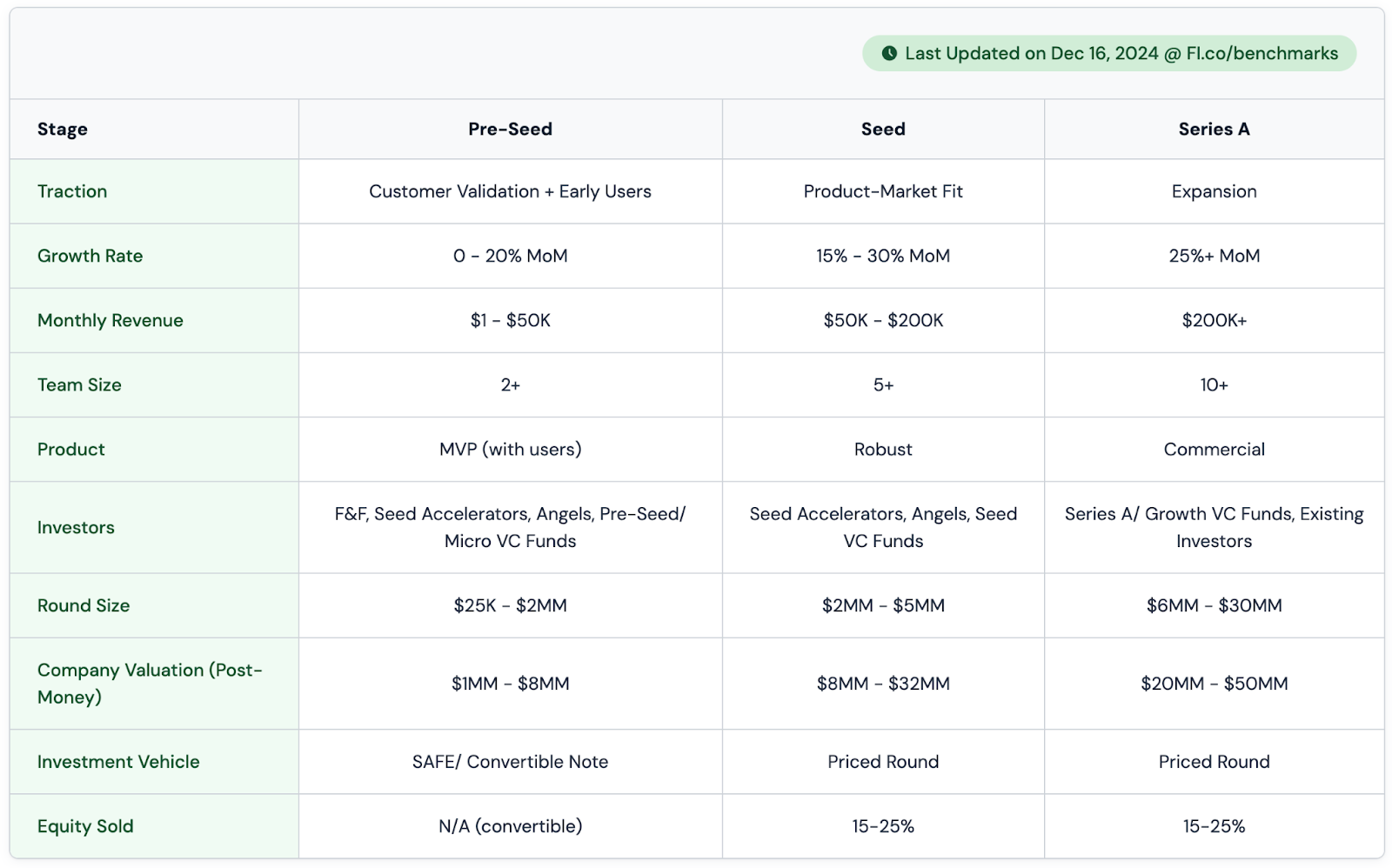

25. Your round terms don't match market standards

As a founder, you may think that your startup is unique. But for investors, your startup is just a financial product they buy on the private equity market.

As for any product, there are market standards.

A $10M pre-seed round isn't market standard. A $100M seed valuation isn't market standard. But also, a $1M seed valuation isn't market standard, and it signals that you don't know what you're doing.

Don't be too high or too low. Unless you are a very special case, just aim for a round size and valuation that are typical for your stage and geography.

Carta, AngelList, FounderInstitute… all produce industry benchmarks that you can use for free. Check out our Valuation page for the links.

26. You're raising under 18 months or above 24 months of runway

VCs expect that the round your raise will last you 18 to 24 months i.e. until you raise the next round.

Does it make sense for your business? Not necessarily. After all, why wouldn't you raise for 1 year or 3 years of runway, depending oin your needs. This 18-24 months period seem pretty arbitrary.

However, it makes sense for the VCs as it signals them that you intend to jump on the “VC treadmill”, where your valuation will get a boost every 2 years, allowing them to mark up their participation, maybe sell some secondaries, and deliver predictable performance to their LPs.

I understand why Brandon would tell founders to escape that narrative.

But that's unrealistic advice for most founders. Unless you are a top 1% founder (previous exit, formidable traction), you can't impose your conditions to VCs.

This is a buyer's market. You have to fit VC expectations if you want to get a deal done.

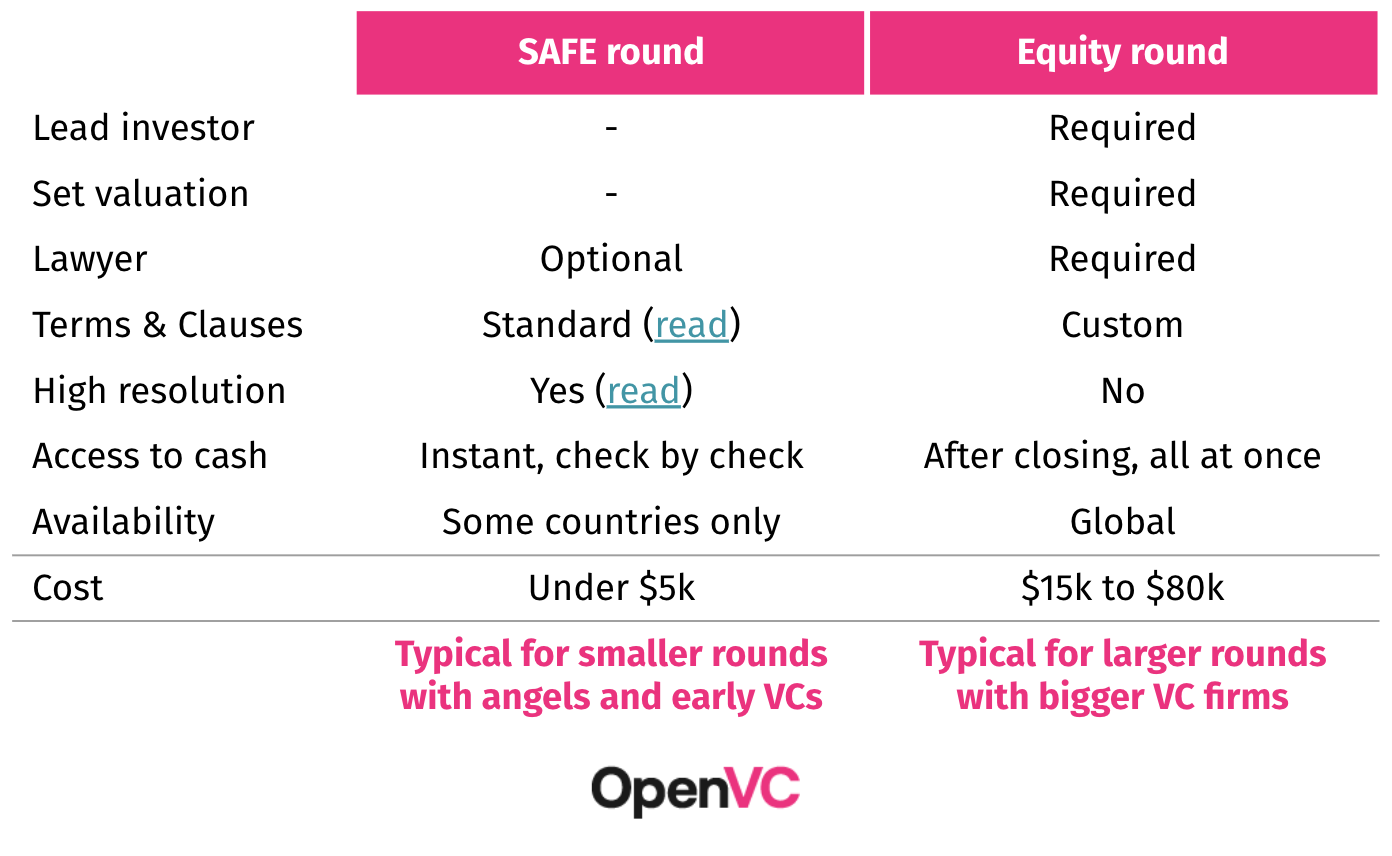

27. You're talking about “equity” and “valuation” at pre-seed

If you're raising less than $2M in most countries, you would likely raise with a SAFE.

A SAFE is a simplified agreement that allows investors to give you cash against the promise of future equity.

Here's the kicker: a SAFE round is technically not a priced round. There is no equity exchanged. There is no valuation set.

Instead, you will discuss “cap”, “floor”, “discount”, and “MFN”.

So when raising your $500k preseed, don't talk about “equity” or “valuation” to an experienced investor, lest you sound ignorant.

28. You can't handle rejection

Some founders just can't keep their emotions in check.

They get rejected, and they either go passive-aggressive (“Your loss, you will regret it”) or even just aggressive (“F*ck you, stupid VC”).

Don't do that.

Your name is everything in this business. And it's a small world. An investor may pass on your seed and lead your Series A. Even if they don't invest, they may still provide value down the road by making intros or sharing information.

Instead, consider each rejection as an opportunity to demonstrate your maturity. Acknowledge politely, say thank you for their time, and most importantly, put the relationship above the deal. Be a pro, not a child.

When you get rejected, reply like this:

Not like that:

29. You're building in a cold market

Not all markets are equal.

Twenty years ago, you were a cool kid if you were building in adtech. Today, adtech will get you blank stares from VCs, who would rather invest in AI.

It is what it is.

As a founder, you just need to know how hot your market is and how it impacts your chances to raise.

30. You have no “unfair advantage”

Having a well-rounded team and a rock-solid business plan is necessary, but it’s not sufficient.

VCs want to be given one clear reason to believe in you.

An unfair advantage. An alpha. An edge.

- You own strategic IP for a specific piece of tech, blocking competitors from offering a similar solution. That's Ring patenting motion-activated cameras for doorbells.

- Your cofounder is a major influencer in the space, giving you instant, massive, exclusive distribution at zero cost. That's Mr Beast launching Feastables.

- You were running the show for your top competitor, so you know all about the market, the product, and the clients. That's Eric Yuan launching Zoom after leaving CISCO.

Most startups don't have an unfair advantage, though.

Having no unfair advantage means you are no better than any other team building in the same market. You might outsmart them, you might outexecute them, but you might not.

All things being equal, an unfair advantage tips the scale in your favor, and that's exactly what investors want.

An unfair advantage also makes for amazing storytelling.

Every cool war story has a secret weapon.

31. You're a Forbes 30 Under 30

Do I need to say more?

The 3 super-signals VCs use to invest in founders

There are dozens of ways to fail, but only a few ways to win.

Super signal #1: Track record of the founding team

Investors love it when the founding team has a strong track record.

There's no official definition for “track record”, but it looks something like this:

- Previous successful exits

- Entrepreneurial experience: scale-up CxO, serial founders

- Work experience in highly selective environments: FAANG, MBB, bulge bracket…

- Graduate from selective programs: Ivy-League, Stanford, MIT, IMM…

- Other notable achievements: major open source contributors, high-profile influencer, recognized subject-matter expert, major awards, ex-professional athletes…

Those decks go to the top of the pile.

Why are investors so biased for track record?

For one thing, early-stage startups have no metrics to show, so it's all about the founding team and their past achievements. For another thing, according to “Super Founders” by Ali Tamaseb, 60% of unicorn founders are repeat founders and 42% of unicorn founders had a previous $10M+ exit. So when it comes to venture capital, past success tends to predict future outcomes.

And so, track records matters.

Super signal #2: Traction

Traction is the other big signal VCs look for. Traction means that the company is growing.

More specifically, investors will look at retention and growth, both leading indicators of product-market fit.

Note that traction is well quantified and standardized by business model.

For example, if you want to raise seed for a social media app, you would be expected to show a Day 1 retention above 40%, a D7 retention above 20%, and a Day 30 retention above 10%, with a DAU/MAU ratio above 20%. For ecommerce, investors would be looking for at least $100k in mGMV, with at least 50% YoY revenue growth.

Basically, show that people come to you and they stick with you.

Super signal #3: Who else is investing

You probably know it - most funds don't lead rounds. They prefer following a lead investor and filling the round.

You may not like it as a founder. However, it's a reasonable value proposition as a financial product for a LP. Some funds even make it their whole strategy: “We index YC/A16Z/Sequoia/ similar accelerators.”

Having a big name (or really, any decent investor) leading your round is a massive positive signal.

Conclusion: don't fight VC signals, embrace them instead

Venture capital is not a science.

You cannot scientifically measure and predict success or failure. That's why investors rely on “signals” to support their judgement.

Think of signals as mental shortcuts, pattern recognition, inferences, or heuristics.

Are signals 100% correct? No.

But is it good enough to be 95% right? Probably yes.

Many founders hate that. They feel that investors who rely on signals are being lazy, shallow, and not doing the job they are paid for.

But that's how the industry rolls. There's just too many projects and too little time.

Don't fight the signals, learn to embrace them instead.

![12 Best Startup Financial Model Templates [Free & Paid]](https://d1pnnwteuly8z3.cloudfront.net/images/177302d9-3657-45b7-ac9d-acf801d83a74/1b029edf-43cf-4bd9-9e37-203f66bf426f.png)